We were very fortunate to have Harry Stebbings, Host of The Twenty Minute VC & SaaStr Podcast, take the stage to chat with Brad Feld, Co-Founder and Managing Director of Foundry Group, about his thoughts on a variety of topics, such as venture capital and culture.

Brad has a ton of experience as an investor, starting when he sold his first company in the early 90s. He provides eye-opening insights on the relationship between CEOs and investors, the trouble with the term “culture,” the role of the Board of Directors, what your board composition should look like and whether or not people are destined to be successful only at certain stages of scale.

Listen on for sage advice from someone with over 30 years of experience.

And if you haven’t heard: SaaStr Annual will be back in 2018, bigger and better than ever! Join 10,000 fellow founders, investors and execs for 3 days of unparalleled networking and epic learnings from SaaS legends like Eric Yuan, Tomasz Tunguz, Chris O’Neill, and Mikkel Svane. If you don’t have tickets, lock in Early Bird pricing today and bring your team from just $999! (All ticket prices go up December 1st.) Get tickets here.

TRANSCRIPT

Presenter: Please welcome podcast celebrity, an avid Mojito fan, SaaStr Podcast’s own Harry Stebbings alongside managing director at the Foundry Group and leader of the Feld Thoughts Community, Brad Feld.

Harry Stebbings: 750 VC interviews, I think, has led me to this one and one with you here.

Brad Feld: You’ve worked hard to get here.

Harry: I’ve worked hard but I don’t interview many VCs so I’m a little bit nervous today. I still don’t know how you managed to dress so much cooler than me despite my age, and look so much younger.

Brad: 100 percent attributed to my wife Annie.

Harry: Single Pringle, that’s my problem. Tinder’s a must for tonight then.

Brad: What’s Tinder?

[laughter]

Brad: It’s one of those apps things, right?

Harry: It’s one of those, yeah. I’ll show you later.

Brad: Is it a SaaS model?

Harry: No. Actually, yeah it is.

[laughter]

Harry: Anyway, enough on Tinder. Let’s start today with anyone who’s lived under a rock and doesn’t know how you came to be the central figure of VC that you have, the key instructor to all my learnings through Venture Deals, third edition, now out. I do have to plug.

Talk to me a little bit about you and provide the context for you and Foundry.

Brad: The superfast version of what I’ve done is, I started a company when I was in school in 1987. I sold that company in 1993 to a public company. I was living in Boston at the time. I took almost all the money that I made from the sale of the company and invested between 1994 and ’96 in 40 companies as an angel investor, 25 to 50 thousand dollars at the time.

I accidentally ended up becoming a VC and a partner with a firm that I helped start originally called Softbank Technology Ventures. It eventually became called Mobius Venture Capital.

We raised three funds. The first one did extremely well. The second one was a complete disaster, and the third one, depending on the outcome of one company, will either make a little money or lose a little money, which, by the way, was a 2000 fund that we’re still managing today. The idea that venture funds last 10 years is a happy fantasy.

Mobius scaled way up in the Internet bubble to about 70 people. We had 10 partners, after the Internet bubble collapsed, it scaled way back down. At 2005 was the end of our investment period, 2006, a group of us decided to start Foundry which we started in 2007. We started Foundry in 2007 and have built from there.

I lived in Boston until 1995. I grew up in Dallas, Texas. In 1995, my wife told me she was moving to Boulder and I could come with her if I wanted to…

Harry: [laughs]

Brad: …and that’s how we ended up in Colorado.

Harry: And you downloaded Tinder. Obviously the conference is based around scaling SaaS companies. I want to start today on something that you’ve spoken about before that was particularly profound for me and it was segmenting the company and the internal structure into three different machines.

I’d love to hear your thoughts on how to structure the internals of the company into these three differing components.

Brad: However many SaaS companies later, let’s say we’ve invested in 50 or so that would be true SaaS businesses. I continuously struggle with the endless organizational change that occurs roughly whenever you double a size of a company. It doesn’t matter what your starting point is.

If you’re a 20 person company, you double to 40, you have to change a bunch of stuff. You go to 80 you have to change a bunch of stuff, 160 you have to change a bunch of stuff. Each time the lens of what you change is usually very dependent on people. You have your org chart, you start talking with this person and scale and this didn’t. You’re in that mix.

I have this continuous mantra of there’s three things that matter. One is the product, which by the way for many years was the only mantra. The only thing that matters is the product, everything else will take care of itself. That turns out to be bullshit. The other stuff matters too…but the product, the customer, and then the company.

I was in a rant about that with somebody and I said, “Why the fuck don’t we just talk about those three things?” I don’t care what the organizational structure is and I don’t need a bunch of fancy words like BDR, SDR, QDR, LDR, like customer machine. What are the cool kids calling a customer service person today? I’m old now.

Then we called them customer service, now they’re customer success. There’s probably some new word for it that’s like obdi gobdi bobdi success because you need a new acronym.

Harry: Of course.

Brad: Instead just focus on these three machines, staff appropriately, and use them at each level of your organization to say, “Are we running our product machine well? Are we running our customer’s machine well? Are we running the company machine well?”

Harry: What does the reporting structure look like with that? Is that the CEO maintaining all of them? Is that having individual heads for each?

Brad: It varies and I would say when I wrote about this a couple of months ago I said I’m clearly playing around with this. It applies by the way not just to SaaS companies, but any of the companies that we’re investing in. The CEO sits on top of it and whether the CEO sits in the machines or not to some degree depends on the scale of the company.

There’s a continuous cliché about should a CEO be working in the company, in the machine or on the company, on the machine? Actually abstracting it out like that causes you to have a deeper conversation about, who should be running the machine, that’s the product machine, and how should the CEO interact with the product machine?

A good challenge for many companies early on is the CEO’s proclivities. Let’s say the founding CEO is a product person. They will spend way too much time in the product too long. In the beginning it’s really necessary, but as the business starts to scale, they have to disconnect from that.

If it’s a salesperson, that person will overcompensate in the customer machine for too long. It’s a very predictable weakness that you see in companies as they hit the 5 million to 10 million ARR level, where all of a sudden, the strength of the CEO in some ways becomes a weakness of the business.

By abstracting the machines away a little bit, it forces you to think more precisely about, is it the CEO and one executive? Are there two executives? Product machines, do the CTO and your VP of engineering run that? How do they run that together?

How do they figure out how to deal with things versus, “Oh, well, we have a VP of product and a VP of engineering and the CTO over here that has a different responsibility”? No, they’re all working on product. Let’s focus that energy on product and figure out how they navigate what they do.

Harry: You said about the scaling earlier being centered to all around the people. I’m intrigued. We often hear that some people are destined for certain stages of a company life cycle. Do you very much agree with that, that some are pre-seed, some are Series C players, or can they have flexibility to transition?

Brad: People can scale if they want to scale. The heuristic that I like to use is that if you’re a CEO of a company, and you’re building your leadership team, and you add somebody to the leadership team, you want somebody who has been in a company that has scaled from 50 percent fewer people to double what you are.

You want that range. You want a person that has that experience, at least. They can have lots of different experiences, but if they haven’t had that experience, they don’t really know where you’ve come from or where you’re going.

The challenge for somebody who joins a company is to be self reflective about what part of that journey they like. The idea that somebody is an excellent VP of engineering when there is a six person company, and is an excellent VP of engineering when it’s a 3,000 person company is a fallacious statement. It doesn’t mean anything.

It’s both sides. It’s the CEO when you’re looking to build your team and continuing to scale your team, all the way down the leadership team. You have room for experimentation as you get further down whatever hierarchy you have.

In those key leadership roles, it’s not that experience is the thing that works. It’s that having recognition of the person knows what they’re going through, and if they don’t, that there’s enough people around them that knows what they’re going through in terms of the scale of the company. It’s not a first time experience for the whole team.

Harry: You said about the core leadership there and then the scaling of the team beyond that. I’m intrigued with one element in particular, and that’s the transparency. Often, when it’s the core team of five people in the room, it’s transparent conversations. With the scaling, do you think transparency is a fundamental core of the company, or are there some elements like fundraising, which can just be destabilizing?

Brad: I don’t think it’s necessarily an absolute. I’m going to use a very deliberate phrase. I hate the phrase “culture.” The phrase “culture” for me is a total cop out on dealing with whatever reality is going on in your world. That’s what it is. It’s like, “I’m going to just take this box. I’m going to put all the shit in the box and call it culture.”

[laughter]

Brad: Really, the interesting phrase is “cultural norms.” The magic about being a startup and having a startup type business is as founders and as early employees, you’re defining the cultural norms.

It doesn’t matter what your cultural norms are. You get to make them whatever you want. If you decide transparency is one of your cultural norms when you’re small, you can continue to evolve what transparency means in the context of your cultural norms as you get bigger.

If you say, “Our culture is we’re transparent,” that’s bullshit because when you’re five people, you can interact differently than when you’re a 5,000 person public company around the notion of transparency, but as a cultural norm, if you’re 5,000 people, that defines a fabric of how you interact inside the company. It’s important to define. It’s not important what the answer is.

Harry: What would you say are your cultural norms then, when you look self reflectively at the very successful partnership that you have now with Foundry?

Brad: Seth, Jason, Ryan, and I, and now our partner, Lindel, who used to be our largest investor, have a set of things we call “Deeply held beliefs.” They’re the fabric of our cultural norm. Over time, we’ve given labels to things that probably didn’t have labels.

A good example of one is that we interact, we’re all equal partners. That’s a cultural norm. We describe how we make decisions, not as consensus, but as each of us having to give up our veto.

It’s the same thing, all four of us agree on something, but it’s very different between saying, “Yeah, OK, Harry. I’ll go along with you,” and “I am not fucking giving up my veto. I don’t want to do this.” They’re very different.

We have a phrase we like to use which is “brutal honesty delivered kindly.” We are brutally honest with each other all the time about everything, but we deliver it kindly. We argue, we disagree, we do our own version of fighting, but it’s very calm, it’s very direct, it’s not passive aggressive or passive behavior, it’s not meant to undermine.

Everybody has a big red button in the middle of their forehead. If you’re in a relationship with someone, your partner knows your big red button, and if your partner wants to manipulate you, they just press your big red button, and if you want to manipulate your partner, you press his or her big red button.

We know our big red buttons on our foreheads and we try really hard not to press them when we’re having conflict. We fuck with each other plenty so we press them when we have chances.

[laughter]

Brad: That’s part of it, too. Last is, when we started, we said, we are good friends, we want to be best friends.

Jason and Ryan were best friends. Seth had worked for me, so we were close but in that boss/subordinate type relationship. We say we’re equal partners and we’re best friends and let’s act like that from the beginning and today it’s very comfortable for us to say that we’re best friends.

An example we use, it’s an easy one. Jason got married a couple of years ago. His three best men were Seth, Ryan, and I. You don’t do that lightly. Those are the kinds of examples of cultural norms. They’re not static, they evolve and they change with stimuli. They’re deeply held but they’re not immutable.

You can change your mind, you can argue about it, and as time passes and things change, you have fit that into the world as well.

Harry: For anyone that hasn’t actually seen Foundry Group’s music video, it’s out there with Lady Gaga and Justin Bieber, I think.

Brad: I can’t sing or dance.

Harry: [laughs]

Brad: This is me dancing. I like to say it’s like playing tennis. For Jewish kids that dance, you just play tennis.

Harry: [laughs]

Brad: If you want to see some of that, the video’s got it.

Harry: I’m intrigued, though. You said about the friendship there between you as partners. Steve Blank wrote, a couple of years ago now, that VCs are not your friends especially with regards to startup founders and the relationship between startup founders and VCs.

What’s your approach to this and the relationship between startup founders and VCs?

Brad: Steve and I are friends. I like Steve a lot. I’ve learned a lot from Steve and I think he’s totally wrong about this.

I think that some VCs are not your friends and I think there are some VCs who culturally interact with entrepreneurs in a way that they shouldn’t be friends. I also think that you can have a VC entrepreneur relationship where you’re extremely close friends.

Both of those can happen and you’ll be successful. I don’t think it’s one or the other. The absolute again, of VCs are not your friends, I don’t think it’s true. I would offer up my own experience in the entrepreneurs that I work with who I’m close friends with as examples.

By the way, entrepreneurs who I have succeeded with and failed with. There’s probably an element of Steve’s own life experience. If his experiences that they color that, that’s correct.

There are some people, on the investor side, who can have that kind of, define what you want by friendship, but an emotionally engaged personal relationship that transcends the business interaction, there are some entrepreneurs who can have that kind of a relationship, and there are plenty of each that can’t.

It depends on the fabric of what the relationship is. It gets more complicated in that most boards and most companies are not one VC and one entrepreneur. Even if we’re good friends and we’re both on the board and you’re the CEO and I’m the investor, there’s other people around the table interacting. The dynamics of the relationship are more nuanced.

Harry: That’s a super interesting thing for me and probably a lot of founders in the audience in terms of evaluating board configuration and establishing that board. How do you look to establish that board and particularly at different stages of company development? Say I’m a seed founder, what does it look like for me?

Brad: This is another place where Steve and I disagree but probably disagree on form but probably agree on substance. I wrote a book about boards called Startup Boards and making your board of directors work for you or something like that, it’s a subtitle.

By the way, writing a book about boards is really tough because it’s really hard to write a book about boards that’s not boring.

Harry: [laughs]

Brad: Of the books I’ve written, I think that was the hardest.

In that book, there’s actually a section where I compare and contrast to something I wrote for some “Wall Street Journal” content thing and Steve wrote about boards. Steve said don’t have a board until you absolutely have to. Delay it as long as humanly possible. Wait as long as you can. Instead of having a board, just have advisers.

I said as an entrepreneur, the experience and lessons that I’ve learned over and over again, I’ve learned it from Techstars almost a thousand times now, is, start the discipline and the rhythm of having a board that you’re accountable to early. It doesn’t mean it has to be investor board, but the rhythm of outside accountability as well as the advice and the help you get from it.

By the way, that early board should be working for you, the CEO, as long as they support you. They’re not judging you, you’re not reporting to them, you’re building a team that’s helping you and part of what that board’s responsibility is to help you succeed and grow especially if you’re a first time entrepreneur.

Different frames of references, same kind of thing. Lots of VCs have different perspectives. Many VCs believe that they’re entitled to a board seat every time they write a check.

Harry: Board seats for sale.

Brad: Board seats for sale. Many entrepreneurs look at that and say, “I’ve got five investors. I don’t want five investors in my board.” You shouldn’t. You shouldn’t have more than one or two investors on your board. It doesn’t mean that those investors can’t have access to the board dynamic, but your board as a CEO and a founder is a precious thing, treat it well.

Harry: What is the composition of that board, then? I may be entering VCs, I’m used to all of them…

Brad: It varies all over the place. Everybody has their absolutes. I won’t do an investment unless I have a board seat. I won’t do an investment unless I have 20 percent of the company. Oops, I did that investment. Oops, I only have six percent of that company.

The natural tendency is you have VCs who are board members who are used to being board members, I’m one of them. I’m on the boards of most of the companies that I’ve invested in. Once you’ve been on a lot of boards and you’ve been to like 10,000 board meetings, you don’t ever have to do it again.

You start thinking about how can I most help this particular company and how can I help this particular set of founders and this particular CEO in the construct of the business they’re trying to build, versus the mentality that I think some investors have, it’s fine to have it, is “My job is to watch over my capital. My job is to play a board role and be the governance of this business. My job is…”

There are plenty of VCs out there still that think the CEOs work for them. I’d suggest that that’s something that someday, probably you’ll be able to point and say, that VC thinks that way and that VC thinks that way, versus the other which is, whether it’s cliché founder friendly or something else, which is, I’m here to work for you.

It’s not because you control all the voting stock but because, as evidenced by the IPOs like Snap and Facebook where really the board is at the behest of the founder, but this dynamic of we’re trying to build something here together. Let’s make sure that we have rules of engagement for how to interact. Let’s focus on that.

Harry: You said that about your 10,000 hours as a board member. When you…

Brad: 10,000 board meetings, not hours. But if they’re all an hour long, I’d probably be…

Harry: Sorry, 10,000 board meetings. With that in mind, and when you self reflect on those, how have you seen yourself develop as a board member over the 20 years or so that you’ve enacted that role?

Brad: When I started being a board member in the mid 90s, I had no idea what a board was. My board experience tended to be linked directly to the boards I was on, and I wouldn’t say deferential to the people who were more experienced, but you get guided by whatever that rhythm is. I would say my world around that broke in 2000, maybe 2001.

As the Internet bubble started to blow up, a couple of things happened at the same time that caused my view to have to change. One was, I was co founder of a handful of the companies I was on the board of, so I straddled an operating role and an investor role, which got really complicated when things got all fucked up.

Second, I was on a lot of boards. I don’t know what the total number is, but let’s say 25/30 boards, which was an untenable number of boards to be on. The third is that the boards were used as the interaction point with the investors. I realized that part of the reason it was untenable is because I had a board meeting every month for every company, and I had too many of them.

When lots of them are going fine you can manage your way through it, but when all of them were completely in the shits, all of a sudden your whole world is every single day you’re dealing with a whole new crisis in a company that nobody’s really paid attention to for 30 days.

Changing that dynamic as a board member to what I like to call today continuous involvement. My job as a board member is to do what the CEO needs me to do, and every CEO is different. Some CEOs for periods of time need to talk every day on the phone, or they need to email back and forth lots of stuff. Other CEOs the last thing in the world they want is to talk to me for another 30 days.

That’s up to them, they get to define. Rules of engagement, again, the terms of the relationship are theirs to define not mine. I think that boards are healthier when the CEO is very clear with the board about what the CEO wants, and it’s not necessarily an absolute. “I never want to have a board meeting, I never want to talk to you board members. Thank you for your money, leave me alone.”

Well, that’s not going to work. It’s a discussion about how to interact in a way that gets the board members engaged on a continuous way. That doesn’t mean that you’re not going to screw things up, you’re not going to have surprises, you’re not going to have crises. That’s all normal.

You have a rhythm so that when those things happen you know how to engage in them constructively rather than reactively. Where everybody’s, “How did that happen? Why did that happen? Why didn’t you tell me that?”

The evolution of going from this place where you hoped everything would be good walking into the board meeting, to this place where you assume that a percentage of everything is fucked up all the time, and instead your job is to help unfuck it.

[laughter]

Harry: There is one element I want to touch on in terms of the discussion between the board and the CEO and the founder. That’s now, in today’s world with the balance of focus on unit economics, and then on growth, we were discussing earlier.

How do you look to balance the two very opposing ideas of cutting those discretionary costs and focusing on profitability, with going for all out growth for the VC returns that quite frankly a lot of LPs require?

Brad: I would challenge the last piece of what you said that LPss required. LPs requir in that if you don’t have the returns then they won’t give you money again. It’s not that they require it. It’s that there is a system and the system is…

Again, the job of a VC is super easy. You take a box of money that our investors give us, and our job is to give them back a bigger box full of more money. As long as we do that legally, we’re doing our job.

If we do nothing, if we don’t go to a board meeting, if we don’t talk to anybody, if we sit in our bunker eating Rice Krispies, and we send them back legally a bigger box of money, they’re going to be happy. What you actually do and how you spend your time is going to vary on that. It lies back directly to your question.

In the venture business, especially as the velocity of information has increased…By the way not dissimilar to our whole lives, information 20/30 years ago was hard to come by no matter what you did. You got your news once a day from the TV or from the newspaper.

As a VC there was so much friction in the communication with the companies, you make a phone call, maybe you get a memo faxed to you, like was the fastest it got to you. The dynamics are so totally different. Part of that pressure is that there’s a lot of ritualized belief that doesn’t get fought hard enough about.

One of those ritualized beliefs is, if you’re venture backed you have to grow at a certain pace because that kind of growth has to generate the returns for the VC.

Harry: And for the next round.

Brad: And for the next round. You have to grow a certain pace so you can get more money, so you can keep growing at a certain pace, you can get more money. Lost in that is then this counter balance. What if you grow at a slower pace and actually made money? There is a balance point.

If you’re growing at one percent a year and making money, from a venture perspective you’re not interesting. If you’re growing at 100 percent a year but spending 500 percent of that revenue to generate the 100 percent, that’s probably not interesting either.

Figuring out where you are on that line, and again, if you go to the product machine and the customer machine, you can generate lots of customers, especially in a recurring revenue model, that then just leak out the bottom. The cliché ish leaky bucket that I’m sure 20 talks are talking about.

If you don’t have the customer machine working it doesn’t matter how fast you’re growing, it’s going to catch up with you eventually. If you have the customer machine working really well, but you can’t find another customer to save your life because your product’s wrong, you’re not going to grow very fast.

If you’re spending a shit load of money because you hired too many people and you can’t get those things working, it’s even harder. Getting those things in balance and not thinking about it as an absolute is really important. I would also say it comes in phases in companies. Many of the successful SaaS companies that we’ve been investors in have hit a stall point.

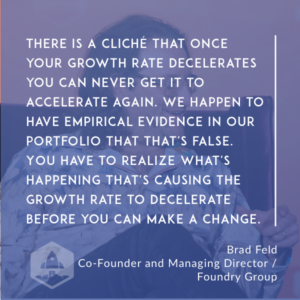

They hit a point where their growth rates slow. There is a cliché, again institutional knowledge in the venture business, that once your growth rate decelerates you can never get it to accelerate again. We happen to have empirical evidence in our portfolio that that’s false.

Now, it’s hard, it’s not automatic, you actually have to do some work, and you have to realize what’s happening that’s causing the growth rate to decelerate before you can make that change. Again, from an entrepreneur’s perspective if you take it as gospel, “Oh, my growth rate is decelerating therefore I’m screwed, I can never raise money again. OK, maybe we should just call it quits.”

You’re not actually dealing with the root cause of what the problem is.

Harry: We’ve got three minutes and nine seconds, and we’ve got five questions for a quick fire round. We’re going to be tight on time.

Brad: I even know what a quick fire round is because I listen to your podcast.

Harry: Thank you so much. You’ve been on it. Let’s start with…

Brad: How many people here listen to Harry? Clap your hands if you listen to Harry.

[applause]

Brad: If you don’t listen to Harry on SaaStr or Twenty Minute VC, listen to him. It’s awesome.

Harry: Thank you. If you haven’t bought Brad’s book then…I learned to do it from there so I mean…

[crosstalk]

Brad: Sell some books would you.

[laughter]

Harry: Sorry, I left it to the last…

Brad: All right quick fire round, two minutes and 40 seconds left

Harry: Let’s go. Why is CAC a nonsense metric?

Brad: Lots of metrics are super easy to game, CAC is probably the easiest. You game it because CAC against LTV has assumptions about what the actual length of time lifetime value is. CAC is essentially direct versus indirect costs and how you think about those things.

The last piece of it, which for me is really telling, if you don’t link any of those kinds of metrics to your actual gross margin that you’re delivering, it’s very, very easy to recognize that you’re selling something that in a SaaS business should cost you 20 percent to deliver.

Your gross margin should be 75 to 85 percent, but you’re actually shoving a bunch of your costs of customer acquisition and customer management into the cost of delivering the product. Really it’s easy to move those around.

Harry: What was the most profound moment for you in 2016, potentially in learning or experience wise?

Brad: Most profound moment was my day in prison. I went to prison for a day with an organization called Defy Ventures. Mark Suster and I sponsored a trip. It’s the first time I went, the second time Mark went, we spent 12 hours in level four maximum security prison, 75 entrepreneurs and VCs and 50 of our newest friends, who we referred to as entrepreneurs in training.

It was a graduation day for a six month incarcerated entrepreneurship program that Defy runs. It wasn’t the best experience of my year, but it was the most profound.

Harry: Let’s finish today with, what would you most like to see change in the world of VC in the coming months and years?

Brad: Nothing.

Harry: Nothing?

Brad: It’s been really good lately.

[laughter]

Harry: In terms of the ecosystem potentially then?

Brad: Fred Wilson wrote a great post yesterday. I don’t know if people saw it, but it was maybe two days ago, he’s like, “We’ve had a great run for the last 25 years,” because he was writing about how net neutrality is going to be over, and the consolidation of power amongst a small number of incumbents, which always changes market forces. It’s not, and we’re doomed.

It’s, and that was a good 25 year run, and now we need to start thinking hard about what the next dynamic is going to be given that the landscape’s wrong. Whether he’s right or wrong is irrelevant, I wouldn’t overreact to it or underreact to it. I think that for me an increased understanding of the non financial, non transactional side of this business is something that is important.

There is two organizations I’ve been involved in that are doing a huge amount of work on this. One is Reboot, Jerry Colonna’s organization, which is in addition to running entrepreneur boot camps runs VC boot camps. Now we’ve done two of them. Also Kauffman Fellows, which is now in its 21st year, has about 45 VCs each year in its program.

I just joined their board, and it’s an organization I was involved in very lightweight because of my relationship with Kauffman Foundation when they started 20 something years ago. I’ve known it from then. I think that notion of VCs are people too, and, by the way the most important person to realize they’re a person is the VC.

To actually do their own work on how to be great at what they do, and how to be great at what they do in the context of the entrepreneurs they work with, I’d like to see more of that in our industry.

Harry: Brad, it’s been absolutely fantastic to have the chance to interview you after probably 24 months waiting to interview you in person, so thank you.

Brad: I’ve known Harry for two years now. This is the first time we’ve seen each other in person. He’s just as young as I thought he was.

[laughter]

Harry: Thanks so much, Brad.