A discussion with SaaStr CEO Jason Lemkin and Keith Rabois, Partner at Founders Fund about the latest on unicorn and decacorn valuations.

Keith Rabois | Partner @ Founders Fund

Jason Lemkin | Founder @ SaaStr

Jason Lemkin:

… For a bunch of reasons. One, it’s an important topic. Two, founders care a lot about Venture maybe more than they should. A fun topic maybe I’ll hit with Keith if we have time, there’s maybe too much interest. But also there’s so much Sony Bologna on Twitter and so much change, right? Are we open for business? Are we not open for business? I almost feel like we’ve gone through three phases in Smartsheet shut down, what’s happening and then rush to the new new. I don’t know what’s going on but I knew I wanted someone that would tell us exactly how it is, speak with data, be unvarnished and have enough wins both operationally as investor under his or her belt to not hide anything, just to share it how it is. So I reached out to Keith so that we could hear that because I think we’re still going through times where it’s hard to get the straight scoop.

We had Christoph Jans this morning from Berlin talking about how you needed a much longer list of investors. You had to talk more people, how people will slowly flake out of a process, how it’s harder to build relationships over Zoom. It’s hard to know what’s going on especially from folks Twitter feed and what they say. That’s what I want to dig in today. Again, on Zoom, there’s a Q and A, so ask questions here. To the extent we have time, I’ll ask as many of Keith as we can and we’ll try to answer as many as possible. So pop into the Q and A. I wanted to dig in into Founders Fund and some tactical stuff but Keith, let’s step back because I know this is something that everyone’s thinking about all of the world, everyone on Twitter, tell me what you’re thinking about how do I get my arms around this slide, right? On the left, we go into February and this is the best of times, isn’t it? 10, 11 years… I mean, it’s better than we ever thought. Right?

There was this joke on Twitter the other day, someone who was pointing out how on your LinkedIn you said PayPal, it exited at a billion and now it’s worth 40 billion or 50 billion. So we figured out a long run, but even before you update your LinkedIn and then bam. Look at this, the BVP Cloud Index we plummeted in March and then as we were talking about before, if you just put all your money just into Square on March 20th, you would have doubled your money, right? Let alone the Datadog and the Shopify guys and the Zooms. And yet, as you’ve talked about all, look at what’s happening in California. I mean, it’s devastating. It’s unprecedented. As an investor and as someone looking forward, how do we weigh the two sides of this, the best and the worst of times?

Keith Rabois:

Yeah. I mean, there’s a couple of potential theoretical answers that would reconcile these two worlds. One is maybe stock markets are longterm investors and all the critiques that public market investors are short term thinkers are just false and you can make a stronger, pure argument right now that all of the major industries in the world are basically taking a long term perspective on the value of these companies, looking at the effectively discount cash flow projections and saying, “Hey, there’s this Virus-Clip that’ll be between one and four quarters long, but nothing about a 20 year horizon has gotten worse and if anything, maybe things are better over 20 years.” So all the people who were whining, jumping up and down about the evils of short-termism and public markets, which I never really believed in any way, maybe you’re just factually wrong. That’s one thesis.

The second way to go is typically, when you do your discounted cashflow for those of you who went to business school or something, you’re basic applying it, the key variables, actually your discount rate and with the effective interest rates being so low, your discount rate is basically negligible. Yeah, I know what discount rate you apply. In some ways, if you just held everything cost in and change your discount rate and reduce it by a meaningful amount, you’re going to get exactly the chart on your left. That actually would work just empirically also. I don’t think it’s that hard to reconcile these things. What’s a little harder to reconcile is what’s going on in Venture. We’ll talk about that separately, which is, I actually do think that most private market investors are somewhere between spooked and reorienting their approach and valuations. And that’s a little bit disconnected from the public markets at the moment. At some point, those things need to be in harmony, at least in partial harmony.

Jason Lemkin:

So let’s come back to that in a second, but just to understand these two. Just to unpack a little bit what you’re saying. At least many SMBs are incredibly impacted, right?

Keith Rabois:

Yeah.

Jason Lemkin:

I mean, the levels of small businesses shut down. Many of which the Shopify in the Squares would attempt to power. Some of them are doing better, don’t get me wrong. But the level of businesses in the tenderloin, the level of businesses is a nap on. I mean, it’s going to be devastating. It’ll be years but many will never reopen. Does it not matter for the chart on the left? Does the unemployment… I mean, just getting away from the human impact, does it not impact at the end? Does it not all bubble up to even the best cloud stocks?

Keith Rabois:

It’s unclear which stocks a ball is up to. I mean, many companies are not really serving the target market of the SMBs that are most affected, think like traditional retail, traditional coffee shops, comfort food, gyms, fitness, et cetera. There are some companies that are technology companies that have to do work with them and do target them but that’s not the meat and potatoes of most companies. The Squares absolutely, Yelp to some extent absolutely. But that’s more the exception than the role of the go to market for many companies. So you could still reconcile those if you had to. Then typically, in a recession and depression, whether we’re in a depression or not open question, but the consumer demand falls apart pretty quickly. And because the driver or the impetus for this economic turmoil wasn’t really lack of consumer confidence or lack of consumer resources, it’s not clear that consumers don’t have the money to spend.

In so far as you’re talking about consumer or pseudo consumer stocks, people have a lot of disposable income at the moment, partially because they’re not spending it on things they normally would. Typically, a normal American goes out to eat a certain number of times a week. That’s expensive. They may take a certain number of Uber’s, that’s expensive. They may go see a movie or two or show or play. They’re not doing any of those things. They’re actually effectively saving money. They have the ability to spend it in other places, whether they spend it now or save it and then spend it once the economy opens again. I think that that will help certainly prop up consumer based stocks. Then on the other hand or on top of that, the government’s obviously subsidizing a lot of people who are suffering and so they don’t feel-

Jason Lemkin:

That’s for sure.

Keith Rabois:

… The short, acute pain. They’re not changing their consumption patterns as dramatically as if they were… I was watching a movie the other night about The Great Depression, that was a true 25, 30% unemployment or 20, 25% unemployment, where there was no consumer spending. And so obviously the people that need consumers to spend money for their revenue and then their contribution margin just had no shot of selling things, look at model T-shirts or something. Right now if you look on the other side, an area I know a fair amount about, look at US real estate. Somehow this defies logic but is true. Last month, housing sales in the US are actually ahead of last year, like literally ahead. That makes no sense in many ways. It’s like 16 depths ahead of last year.

There is in another tale two cities is most of the people that were most affected by the March and April shutdowns were not the people that buy and sell houses. They’re people who typically are 1099 workers with lower fiber scores or lower income. And so it didn’t affect the US real estate market, except for like two to three weeks where everything was shut down and just couldn’t transact. But right now, I mean, Redfin has published several studies publicly about how they’re ahead of last year. Zillow, I saw this morning is trading at probably at 52-week high. People are buying and selling houses. That suggest that there is this weird combination of something’s thriving and something’s failing. I think the music industry, for example, at the extreme other end is catastrophically affected. The idea that people are going to go see live shows in dense environments with worst sanitation or they’re going to… I just think that that whole industry doesn’t know what to do in itself at the moment and it’s going to take years to sort that out.

Jason Lemkin:

Since you’re maybe spending more time looking at some of the consumer data than many of us are, it sounds like there is some hints of optimism in what you’re saying and that maybe you think… And we won’t hold you to this if in July you change your mind. We’re all learning. But it sounds like you feel like there’ll be a decent V. The $10 trillion being deployed to prop up the economy and pent up consumer demand may create a weird V, but it may create a V that’s reflective of the chart on the left for consumers.

Keith Rabois:

No, I think it’s going to be more inconsistent. I think by segment. There’ll be some Vs and then there’ll be some complete flat-lining. I think it’s more overall more like 2000 to 2003 in Silicon Valley, but there’ll be some industries and celebrated goals that either aren’t effected as much or snap back very quickly. And then there’s going to be others that take years. There’s a stat I saw after 9/11. Just before 9/11 occurred, we’d hit a USP domestic travel record and it took three years until May 2004 to get back to the level. I think many industries will be like that, where it takes two or three years to get back to the same level. I think some businesses never get back to the same level.

I think international travel is almost permanently affected. Permanently meaning measured in three to 10 year doses, aware of the idea that you can just travel almost anywhere in the globe on a whim is not going to happen. Countries are going to take their borders very seriously. There’s going to be different rules, and different processes, and different tasks and different paperwork you need to travel. Every time you add friction of getting paperwork, tasks, et cetera, less people are going to travel. The idea of a weekend trip from New York, people live in New York, a weekend trip to London probably that’s not going to happen for a very long time. Those industries and the associated industries, hospitality, et cetera, I think are in for a very long non V-shaped recovery. Whereas some industries I can see snapping back, maybe long tail retail definitely. I already see this.

I’m a multiple time investor in a company called [Fair 00:11:21] that basically provides data and services to SMBs all across the US and gives them the tools to compete with Amazon. The company was doing phenomenally well and our customers were doing phenomenally well before March hit. We clearly saw the impact the first three weeks. It’s dramatic. Nobody can go shop in main street America. But in the last three to four weeks, there’s been a sustained week to week improvement. I suspect-

Jason Lemkin:

In store. [crosstalk 00:11:49]

Keith Rabois:

… Well, there’s some substitution. That’s a fair caveat. Some of these businesses, maybe even many of these businesses have started investing more and more in selling online to their preexisting in store customers. They’ve been actually quite clever and scrappy and figured out how to offset the decline of revenue. But then now the fact is now in May, likely to be more like a 10 to 20% net. Well, actually that’s even wrong. The company will grow more than two actual year to year in that despite all the lockdowns. There is definitely a sustained improvement across the country. Inconsistent, they serve the virtue of having 70,000 retailers or something like that is you actually literally have retailers everywhere. And so yes, in San Francisco, they’re probably not selling that much and in LA, probably not selling that much but somewhere in Nebraska, they’re probably back to normal.

Jasom Lemkin:

Yeah. The pieces that recover at which pace is interesting I wrote. I looked a little while ago and I wrote an early Sastry post in 2013. After I sold EchoSign Adobe, I went back and got out. I rented a small office in downtown Palo Alto, and it was middle of 2013 when the last boards came down on a retail store. The West Elm store, I don’t know if you know where it is. It’s near Wahlburgers.

Keith Rabois:

Yes, of course.

Jasom Lemkin:

I was boarded up until 2013. That sounds crazy thinking about it, doesn’t it?

Keith Rabois:

Yeah.

Jasom Lemkin:

2013 had been boarded up.

Keith Rabois:

The lag is very real. Then also, there’s industries where it’s just hard to follow them how they deal, from an economic standpoint, with either consumer or government mandated density caps. Like think restaurants, hard to imagine how the economics of those businesses work with half the tables.

Jasom Lemkin:

Let me just ask you on this one. I want to hit the next slide. Pick your date in February, whatever it doesn’t really matter, where were we overall in Venture one to 10? Say on February 15th or February 1st, where were we on one to 10?

Keith Rabois:

I think we were already down to a six or seven. ,

Jasom Lemkin:

Oh, really?

Keith Rabois:

Yeah, I think some of the corrections in valuation, enthusiasm tolerance for high burn rates and things of that sort, had already been adjusting or were adjusted for the last six to nine months. Somewhat, I would tie it back if you had to put a kind of opinion timeline right around that we worked the debacle is when I think there’s a very clear retrenchment, repricing, re-analysis of what’s the right criteria for a growth around. For example Founders Fund, I don’t think we changed our criteria at all, but I felt like maybe we were on the 20th percentile in terms of conservatism on some of these metrics. I felt like everybody moved to agree with our metrics and goals and objectives very quickly, where maybe there’d be a 10% of people who had still fund stuff that we thought it was a miserable business from an empirical standpoint. It really did move from 80% fund stuff that we didn’t like to only 10% of people would fund stuff we didn’t like. [crosstalk 00:15:11].

Jasom Lemkin:

We may look back that we work IPO is the moment when things changed. Right? And when that was whenever one, we didn’t see it all, but that might’ve been a moment.

Keith Rabois:

I think that was always clear to people. It started to change before that, truthfully, at least in my view from my Venture point. But I think that was when everybody had the proverbial partner meeting discussions about what are we funding, why are we funding, what price are we funding. It was a crystallizing moment even if some of that stuff already had some momentum behind it.

Jasom Lemkin:

If we were a six and a seven there, and that’s good, from a very narrow SaaS perspective, I would have rated it at 11 but I don’t disagree with you [inaudible 00:15:54].

Keith Rabois:

Sure.

Jasom Lemkin:

Where are we today from your perspective if different from Founders Fund, if that was a six or seven, not March, not April, but wherever the heck we are today, May 27th?

Keith Rabois:

Maybe like a three.

Jasom Lemkin:

You think it’s a three?

Keith Rabois:

Yeah. I think there’s deals being announced. I mean, including IAA and now four investments over the last month, let’s say. But almost all of those have significant momentum, at least maybe a handshake, cost of a term sheet, maybe even signed documents before March 16th. Then it takes a while to get through the process of negotiation, real documents, wiring money, [crosstalk 00:16:38]. Yeah. All that stuff at large. I think that the reality is very few new deals are getting done with very few exceptions. I think there are some growth rounds that are getting done because you can look at the spreadsheets and these are pretty impressive businesses. There’s a handful of businesses that just look amazing on paper. They look amazing on Excel or paper or whatever, Excel spreadsheets or something.

Those deals are possible to do, especially with public market comparables being both high and no longer quite as volatile. I mean, just feel some volatility. You could just even look at today, there’s some volatility in the market. But it’s pretty easy to hit the outlier high growth companies with moderate bird, batch payback on a cap basis. Everybody wants to invest in it or most funds are looking into those. And so those deals can still get done. The earliest stage stop, I would probably guesstimate is getting done at 10 to 15% normal in terms of velocity and probably-

Jasom Lemkin:

That’s a lot different than you’d think looking at the press, right? 10 to 15%?

Keith Rabois:

… Oh yeah, absolutely.

Jasom Lemkin:

A lot different.

Keith Rabois:

I mean, 10 to 15% and add probably call it 50% of the valuation of last year.

Jasom Lemkin:

If you’re growing faster than March 15th, how does that impact that calculation?

Keith Rabois:

If you’re going faster in a way where also the unit economics/payback is improving and that’s actually true for some companies, like think DoorDash or some telemedicine companies as extreme examples, those are pretty fundable for two reasons or home fitness in some ways maybe. I’m not sure whether the payback on the home fitness thing has changed that dramatically, the cut payback, but certainly the growth is there. Those companies are very fundable right now because basically, it’s like a version of the old why now question. So every good investor deck has as a white house slide. The postmark 16th is just amplifying that question. Why is your company better post COVID? If you have a great answer to that, people will definitely be interested in funding you. It’s species of the old canonical Why now question. But if you don’t have a great why now question, then I think you’re getting lost in a quicksand in VCs that are polite but not really investing.

Jasom Lemkin:

Yeah. Let me just dig into that a little bit. I think this was the point you were trying to make with Fair, that it’s still doing incredibly well, just not quite as well as it would have done absent COVID-19, right? [crosstalk 00:19:19] instead of 3X.

Keith Rabois:

Yeah, good. Literally, our plan for the year was to grow or plan for 2020 would be to grow more than 3X, which is great. I mean, for a company that had pretty good scale. But we’ll still put up two backs even with COVID, which by most metrics that’s a pretty good year. Maybe not be good enough for the company’s ambitions, but we’ll get back tO 3X. But 2X year to year is actually not that bad in the grand scheme of life.

Jasom Lemkin:

Not that bad. Let me ask the question then for new deals and as you said, you’ve announced a ton of deals personally in the Founders Fund, but most of them were in flight before all this happened. One way or another in flight.

Keith Rabois:

Yeah.

Jasom Lemkin:

For a new deal, that is like a fair. Maybe not literally fair, but let’s say in February you were at 2 million ARR tripling and you love the Founder. Okay? It was in a good space, it’s growing 3X, unit economics are plenty good. Whatever your bar is, your bar is high but tripling, quadrupling going 2.5X and instead of 3X, now it’s 2X or instead of 3X, now it’s 1.8 X and it’s not [inaudible 00:20:29]. So, it’s not restaurants. Do you just do the deal? Do you just connect the dots and say, “I’m going long. I don’t really care if it’s eight to 20 months until this recovers.” Or what’s the honest answer for you and Founders Find? Is it still tough to make that mental leap that it’s just a gap?

Keith Rabois:

I think it depends on how much is this a temporary blip. Meaning can you articulate. Look, everybody’s going to have a weird set of metrics in late March, early April. Typically, when we’re funding a later stage company, they have this super smooth growth curve and everything looks amazing. Very few people are going to be presenting for the next year or two slides that are perfect. Everybody’s going to have some volatility, at least in March and April. And so you can show that the volatility segment of time or time is pretty temporal and that you’re back on a predictable growth rate, et cetera, even if it’s a month or two, three months of that. I think there’ll be some serious interest in investing in companies like that.

I think you get basically a pass. In most company here you get a pass between March and maybe May in some of their metrics, but the metrics before that pass is on better be pretty damn good and at some point after that pass on, they now start looking good again. If you can do that, I think people would just close their eyes to this middle [inaudible 00:22:02] we’re typically in a growth out and even a series of C can’t really get away with that. A missed quarter looks terrible typically. Everybody’s going to have a missed quarter or so.

Jasom Lemkin:

Got it. But for what I call them, the COVID beneficiaries, the COVID impacted and the COVID we don’t need you anymore. For the impact that I think you’re saying, look, it is hard. It’s a fact that it’s hard. Even if intellectually you know that these industries are coming back, you have to resume growth in two, three it sounds like, to get funded. You have to resume your normal growth.

Keith Rabois:

Yeah. I think you do need to show that if you want more money, that the company has either figured out or at least the macro world has adjusted and so you’re back on whatever trajectory you’re on. Or the company has figured out how to tune what it does, whether in small tuning or large pivoting to the new world and that there’s evidence that whatever adjustments you made are working. If not that, then I think there’s not a lot of appetite to fund companies, especially if they’ve already raised a sizeable chunk of capital. It’s much easier and let’s say to raise sizable chunks, let’s call it 10 million or more. If you’re not able to show that the world has been fixed from whatever perspective advantage point you’re in business or you fixed your company to take advantage of the new world, it’s much easier to past at somebody who’s already raised a dose of capital. Just say, I’d rather take a shot at something new that’s built from the ground up in this new world.

Jasom Lemkin:

Yeah. Then I want to make sure we have time for a couple points. But let me ask you a question that I’ve thought a lot about but you may have much better data and thinking, which is my gut and I don’t have the data to support this but I have my anecdotal data. I’ve made 25 investments and I talked to a lot of founders. I think 15 to 20% of SaaS companies that we work with are COVID beneficiaries. 15 to 20% are in collaboration, sharing E-Learning, even just e-commerce. I invested in a company called Gorgeous, which is a contact center for SMBs on Shopify. March was rough. April it grew 70%. That was an unexpected one. If 15 to 20% are COVID beneficiaries, can that absorb all the ventured capital? Does venture capital even need to bother? Venture capital, no matter how it looks, it’s not a huge asset class. Is it? Is there even any point for new investments in doing anything but a COVID beneficiary?

Keith Rabois:

You could rarely argue that because if you believe that there’s a fundamental shift in the world in any way towards e-commerce verticals, towards ad foam, fitness training, et cetera, absolutely, it would make sense to take your money and only invest in COVID beneficiaries. There’s a big argument. We debate internally all the time. You can debate publicly. How much does human behavior snap back into traditional norms or is there a “new normal”?

Jasom Lemkin:

Now what’s the answer?

Keith Rabois:

Well, I actually think it varies by vertical. I actually think that there are some things that have had a permanent change and people are not going to go back. For example, let’s talk about telemedicine just because it’s easy to grow. Telemedicine had been growing nicely for the last five to seven years. I mean, there’s a couple public companies, several private companies, but it had step function. What I mean step function, I’ll give you some real numbers. Stanford Hospital went from roughly 1700 telemedicine consults a day to 74,000 a day. Cleveland Clinic has roughly the same scale there. So massive step function.

What’s happened is people realize actually, you know what, telemedicine is actually better. I don’t want to go to a doctor’s office where everybody else there has germs or something. I have to sit in this waiting room and the doctor’s never on time whereas mostly 50 to 70% of things that go wrong with me, the doctor can easily diagnose or triage by a telephone call from my home when I haven’t even had a community where let alone to get exposed to other people’s germs. And by the way, they’re probably on time for the telemedicine cough. That I don’t think flips back at all.

Also, the companies, at least the private companies get better marginal economics. I run a telemedicine wave. The regulators also stepped in and made things easier, relaxed some cross state border restrictions on practicing medicine. Unfortunately, I suspect they’ll go back to normal and insist the California doctors could only treat people that are in California, which makes no sense, but they had suspended that which also allowed for this growth. But maybe even the regulators will cave now. I’m sure there’s no, maybe not no, but almost trivial negligible examples of California doctors either really screwing up the practice of medicine for Virginia residents. All of that is just a permanent change. Then you can even see, well, maybe if that’s true, maybe there’s applications that caused him to other versions or species of medical care where telemedicine or quality telemedicine takes off as well.

There’s some things that I don’t think are complete substitutes and really are unfortunate inferior substitutes. You can argue some of the… Even if you go into a home fitness, break this down, I think Peloton is a pretty good substitute for SoulCycle for many people. Maybe superior, cost-effective, more convenient, more adoptable to their schedule, et cetera. I’m not sure the ad home equivalent of weight training is for going to a gym. Most people are not going to have the same equipment, the space, et cetera. We funded a company that provides a really good ad home experience called Tempo for straight training. But to some extent, there’s limits on what you can do in a normal person’s house in America or apartment. I think that is a function of what’s the healthcare situation in estates, what’s the risk tolerance of people were getting exposed to germs. But are people going to permanently stay away from gyms if the healthcare crisis alleviates? I doubt it.

Jasom Lemkin:

Georgia doesn’t suggest it.

Keith Rabois:

No, that’s true. Truthfully, the facts in Georgia don’t suggest that it’s as big a problem as people thought. But yeah, I personally wouldn’t want to be in a gym right now with a lot of other people. It’s just hard to keep everything perfectly sanitized all day long, even if you put density caps on. But I would imagine, you’ll see gyms, even the equinoxes of the world where you have to schedule your workout.

Jasom Lemkin:

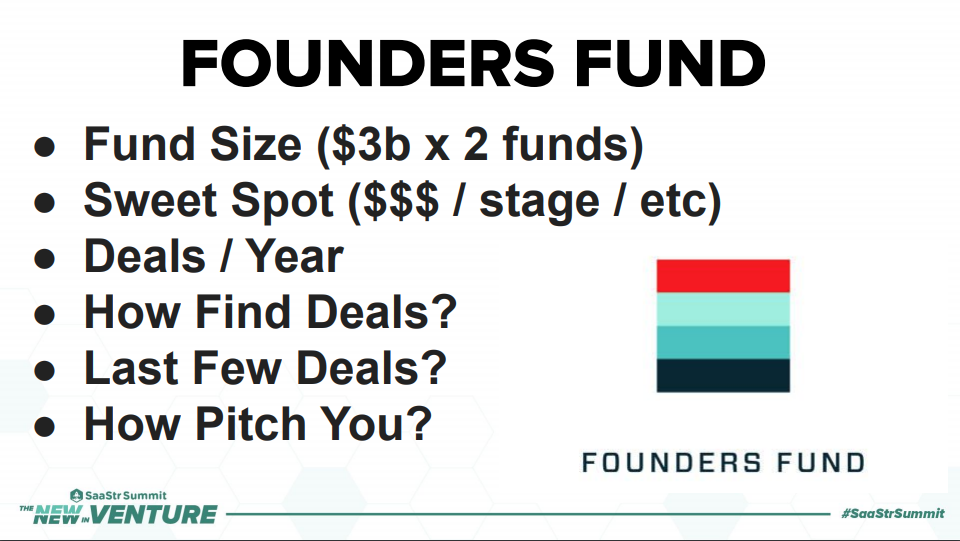

Yeah. It’s complicated. Before we run out at a time, let me just talk a little bit about Founders Fund and you as an investor. I want us to just take advantage of having you to understand how fun investing actually works for a minute because I think it’s interesting. We can talk about whether it’s really changed today but I don’t think it’s changed that much. Let’s start for a minute. You guys just raised $3 billion, right?

Keith Rabois:

Yeah.

Jasom Lemkin:

And perhaps the time [inaudible 00:29:33] with winter typically, maybe not, but you joined $3 billion and your last deal was $8 million or something. The last check that I saw, Run The World was $8 million.

Keith Rabois:

Yeah. I saved-

Jasom Lemkin:

How does that-

Keith Rabois:

Sorry.

Jasom Lemkin:

Yeah, go ahead.

Keith Rabois:

You’re right. We raised $3 billion. We announced it earlier this year, really raised it mostly late last year. We divided into two funds, which is pretty important. The first fund is about 1.4 billion and that’s the Traditional Venture Fund. Then we added a growth opportunity fund of the other half, basically, which is designed for late stage investments, very large rounds, pretty high valuation companies. That’s new for us.

Jasom Lemkin:

And that’s the same GPs and same LPs in both?

Keith Rabois:

It’s the exact same GPS currently. There is some difference in the LP base mostly because we were able to fortunately bring in some new LPs. The Venture Funds we’ve had the benefit of having done fairly well historically. There’s not a lot of allocation or availability for new LPs but we were able to bring on some really top tier new LPs into the growth fund so it’s not the same. We’ll see where we deploy the growth fund is a work in progress. It’s somewhat opportunistic. We’ll see where there’s sweet spots and vacuums in the market and have the capital take advantage of that. With Venture Fund, Founders Funds, this is Founders Fund seven. We’ve been doing this for a while collectively, at least. We started to know mostly what we want to be doing. We did just announce of that. Actually, we only invested 4.6 million, I believe of that round. It’s even smaller than the eight. That could still work though for $1.4 billion fund for a couple of reasons.

One, if the company is doing well, even if we did nothing, but our pro rata along the way, which is not our style by the way but if we did, we wind up with a measure over the next two or three rounds. For example, I’ll give you some data back at my KV, when I was at Khosla for six years, Khosla Ventures, I led the seed investment in DoorDash and never let another round, but overall because KV continued to do our pro rata in each of the next four or five rounds KV as well, North of $30 million invested in the company, even though the initial investment was 750,000 to a million dollars. But if the company does really well and you continue to have conviction and do at least your pro rata you can wind up with a pretty reasonable exposure, but at Founders fund, we tend not to do that. We tend to double down or triple down. Instead of doing pro rata on the way, we will typically like to “power money” into the company and lead subsequent rounds. To some extent, maybe we only invested 4.6 million now, but if the company continues to progress the next round, maybe we would lead with a 10, $15 million chat even the round thereafter. Then with the new growth fund, we could lead the 100 million, $200 million financing on it.

Jasom Lemkin:

I got it. That’s a good case study because it might be a piece of that that’s non-traditional, that’s worth folks quickly learning about. I would say my rough rule for most funds is look at the fund size and it’s important to understand Founders Fund has to split it in half because only half is the Venture Fund. So don’t do the math on 3 billion, do the math on 1.4 billion. But for most partners that spend a lot of the winters skiing in Yellowstone and have a lot of their things going on, a check much less than 1.5% of the fund is going to be tough. It’s not going to move the needle in terms of cash deployment.

Even if a DoorDash, it could make you an insane amount of money, just doesn’t move the needle in terms of their quota. So typically I say, if you’re meeting with a billion dollar fund, they’re going to want to write a 15 to $20 million check to build or start the relationship. You’re suggesting different math that you’ll start earlier, do more work. I think though, that’s a little non-traditional. Will all the partners do it. Is that pretty common?

Keith Rabois:

It is non-traditional to start. That’s clearly right. I mean, At Khosla Ventures where I spent six years before my last year or so at Founders Fund, we would not do that.

Jasom Lemkin:

You wouldn’t do that.

Keith Rabois:

No, we wouldn’t

Jasom Lemkin:

Khosla did see checks but maybe they experiments are small things or…

Keith Rabois:

We did do see checks but they were typically designed to get a reasonable amount of ownership in seed and then we would follow it in an A or try to lead an A. But after that, we were using other people’s money and might make to pro rata but we definitely didn’t want to be doubling down, tripling down. But for the Founders Fund, across several funds now, but we have 17 companies where we’ve invested $200 million or more across multiple funds. We concentrated in positions. It’s one of the biggest differences at least from an LP perspective of how we invest, as if we like the company, we have incredible conviction and this is even before we had growth fund. So I suspect that we will have many more than 17 in the above or 200 million will be the low end, where we have significant dollars invested in a position. But that is very typical.

I wouldn’t count on… I think your guidance to Founders is completely accurate that it wouldn’t make sense to take a million or $2 million or even a position for a million or $2 million from a traditional billion dollar plus fund. It just doesn’t make a lot of sense. I tend to personally like to meet seed investments for three or four reasons. Even though I’m helping quarterback for one point $4 billion Venture Fund, my ideal investment is one to $3 million. That was [inaudible 00:35:46]. Actually at KV too, I had a little bit stricter standard on the ownership for the one to 3 million at KV because I knew we would eventually get diluted downwards and Founders Fund we might actually buy up. So I have a little bit less ownership mentality or handcuffs on me to lead this rounds but I would prefer to be doing one to three, one to $4 million checks all day long. If I could avoid doing other investments, I’d actually be thrilled.

Jasom Lemkin:

Yeah. Some of them might even be personality based as well as economics, right?

Keith Rabois:

Yeah.

Jasom Lemkin:

It is how it works.

Keith Rabois:

Among the reasons why I prefer to be writing one to three or $4 million dollar check is first of all, psychological satisfaction to me in terms of impact to the company. Writing a $200 million check into the next Airbnb when everything’s already working perfectly, they make you a lot of money as an investor but it certainly doesn’t psychologically invigorate me anyway. Secondly, I actually am a Founder driven investor so 90% of my decision or 85% of my decision is based upon the skills and the attributes of the founding team. I’d rather be competing on that to mention before there’s any metrics, because it basically leaves all the other investors without the safety net.

Then third is obviously there’s a risk reward equation in Venture. If you’re right, you want to be really right and say the earlier you’re getting involved, the better that looks as to I’d rather fund things before other people realize they’re good because one way or the other, we’ll get compensated for that. Then fourth is, maybe a little more subtle, when you inherit a company later, it’s a little bit concrete. Concrete is very malleable when it’s in liquid form and you can shape it. Once it solidifies, it’s extremely expensive, wild and destructive to change concrete. So the earlier we get involved, hopefully we can help avoid unnecessary mistakes versus inheriting this die being cast in a solid form where you’re distracted, fixing prior mistakes. Prior mistakes at a top table, prior mistakes and go to market, prior mistakes in hiring to avoid those mistakes and try to be off the races without any unforced errors.

Jasom Lemkin:

Let me ask you an inside baseball question on that strategy of going in seed, which is very attractive. I get Keith to help me early and then leaning in. So if it goes well, lead the next round, maybe even lead the next three rounds. Whatever it is. Is that a negative if things don’t go perfectly? There’s nothing easier than when you’re existing investor, than when your Accelerus Sequoia sends you an email saying, “We’ll lead the next [inaudible 00:38:34]. Don’t bother doing all the diligence, and young woman we’ll do it for you.” It’s so appealing as a Founder but I can think of a few cases where it’s turned out to be a negative. The concentration gets so high and you hit a bump and you end up with a dis-alignment you might not have had if Keith was also on your board as well as someone else or if you had two or three people in that meeting.

Keith Rabois:

Well, I think there’s several components to answer that question because obviously, it’s a complicated topic. I’d say there’s two scenarios where it doesn’t matter at all. One is called the eight, eight plus performance scenario.

Jasom Lemkin:

Doesn’t matter. Nothing matters.

Keith Rabois:

It doesn’t matter. Everybody knows you’re kicking ass and everybody wants to fund you. And then there’s the C minus performance when it really doesn’t matter because nobody’s going to find you regardless of the situation. So you’re really talking about the B zone in the B to B plus maybe A minus zone of when it might matter. To be fair, the bell curve distribution of performance suggests there’s a lot of companies in that part of the curve. The way I think that matters though or not matters lost and sometimes people realize is there’s benefits to having a talented investor who really understands your business involved in the company because they can help you problem solve the reasons why it’s being perceived as let’s say a B or B plus versus an A minus or A, and ideally with enough time to fix it.

One of the most value added things a really good investor can do is with a year or two advanced warning, isolate for you how your company is going to be perceived by other sources of capital. With a year or two, 12 to 24 months warning, you have enough time and leverage at your control to make changes and edit so that you look more appealing versus getting blindsided. When you find out, when you go out to pitch people, when you need money in the next year and the critiques start raining down on you, it’s too late to fix most things. You don’t have enough time, bandwidth capital to fix it. One of the best things a great investor can do is accurately forecast for you what you need to look like well into the future.

The way I typically will do that is I will give them two targets. One is, this is going to be a no brainer. If you can achieve X, Y, and Z everybody’s going to love you. They’d be easiest possible finance saying, “I’d love to invest more.” Other people will be calling you and dailies you with emails. Then here’s the minimum viable financing targets. Where with a lot of work and us crafting a deck together and setting this up and targeting the right VCs, we can get a financing done. And so that they have complete visibility into where they need the land the company, with enough time to land it there. Then what we’ll do is let’s say the landing closer to the B level, we will work very carefully in crafting the deck with Founders. Certainly at KV, I would spend six weeks per deck, per company editing the deck to make sure the story was as polished as possible given the facts and also help isolate which investors on the planet are most likely to resonate with this story.

If you do those two things as a board member, you’ve really increase the odds of success for the company even if the facts aren’t perfect. That offsets some of the potential signaling negatives if you can help place the company in the hands of the right investors who are really going to appreciate what’s working and then help frame the story in the way that makes it attractive knowing who’s on the other side of the table and what their criteria is. I think those two things can be extraordinarily valuable. I watched this as a board member and executive and learn this from the other side, the first 13 years of my career, watching really good board members be able to do this for me.

Jasom Lemkin:

Yeah. Just for fun, and I want to make sure with our last bit of time we talk about your last few deals and how people find you because I think it’s interesting. Even if it isn’t interesting, it’s interesting. But can you think of an investment you’ve done that was a B that only got funded barely due to great packaging and then became an A plus? I’m sure there’s many or maybe there’s none, right? But what some other that went through that phase transition that would be a slightly inspiring story during shelter? Can you think of one?

Keith Rabois:

Great question. Yes. Well, I think Jury Store onto whether they’ll be great companies but I can definitely think of a few that the deck made all the difference in the world. It would have been very easy for me to pass or other people to pass before the company was able to really nail and frame everything. There’s one in specific I’m thinking which I won’t name because they’re out raising money at some point but I first passed on and then a month later they came back with some evidence and with a really good DAC for a very complicated story. And I immediately decided to invest additionally in the C then in A and actually wound up leading there C. So didn’t do the B.

It’s very possible to reframe things in a way and calibrate them. I think here in another version of this, maybe that’s more actionable because that’s an abstract, very complicated topper what makes it a great DAC. But there was a company I’m thinking of right now where it would be incredibly controversial to fund. There’s just so many things in criticisms one could level even though there’s a lot of upside and a lot of positives that my feedback to that founder was you need to meet only the four or five or senior GPS and sort them out because the only people who possibly-

Jasom Lemkin:

No one else can do the check, right?

Keith Rabois:

… Nobody else would do this because they’re going to go to a partnership meeting and there’s going to be so many inbound missiles critiquing this that there’s no way that it gets approved. You need to go to Peter Fenton to benchmark and get him convinced that he must do this. You need to find the other four or five funds that if they long something it’s actually realistic to get funded. It turned out is actually exactly what happened, which is most of the more junior partners in the world hated the company, even though it was liked, it wound up getting sabotaged by their partners. There’s a few fairly senior people who could immediately appreciate what was potentially special but that level of precision can A say found us a lot of time but B also make it more likely to succeed.

There’s some funds where if you go to the wrong [inaudible 00:45:49] you’re screwed whether they have an internal policy about you can’t form shop, once you pitch somebody or just there’s email threads that are particularly on favorable. That’s not true at Founders Fund and that’s definitely not true at KV. We are pretty open minded on people finding the right partner for them but there’s definitely funds that are really good funds where you pitch one partner and they say no, you’re basically done. So even getting to the right person increases the odds because other people are going to say no.

Jasom Lemkin:

Yeah, attribution’s a topic we’re run out of time for today but it is an important one, especially outside of a handful of funds. Before we run out of time, let’s just talk about this. You’ve invested a lot of time in New York and getting out there and being in front of founders. You’re investing time today. You do a lot of work on this whether it’s marketing or PR, you could tell me, but you invest time, right? Even though you are an iconic part of Silicon Valley, you invest the time. How do you find deals? What percent of deals do you not see? Do you ever looked back in Gmail or in whatever half-baked CRM people try to use and say, “Well, I didn’t see that one.” How do you find them and how many do you miss?

Keith Rabois:

Great question. Well, let’s start with the back end of the question first. For me, all the biggest mistakes I’ve made in my investing career are first meetings that I didn’t take.

Jasom Lemkin:

They were there and you just didn’t do it, right?

Keith Rabois:

Yeah, I didn’t prioritize them or turn them down. I’ve actually surprisingly, and this may sound ridiculous, but it’s actually really true, almost never made the wrong decisions at a meeting that I actually took. I can definitely count those and there they’re less than three over 20 years. But definitely filtering some people incorrectly and not taking meeting, few Pretty massive mistake. It’s there and it’s hard. I mean, you get so many introductions emails, you can’t meet them all. You literally can’t meet them all and especially if you’re focused on seed, like what are you going on in that email. There’s not a lot of raw material there. As a result of that at the margin, I’d prefer to take more meetings than less but you still can’t take the all. If you do take too many, I think your brain is also just dead. If you take too many meetings per day and your brain is just not sharp, you’re a little cynical, skeptical, you’re tired so you may miss things in any way. You certainly don’t present that well to founders. That’s one of the hardest things about seed and series A investing.

Series B and later, I think the set of interesting companies is pretty well defined and you can actually exhaustively “cover” or meet them. There’s a KV we’re pretty stringent at tracking this. The way I would track it and redo it on a quarterly basis basically, is I would look at all the announced deals which obviously lie unfortunately, but all the announced deals and basically, just look for the ones that I found interesting and hadn’t met. So we look up. This week we track 10 funds that were our closest competitors, look at all their announced deals and then go back to our CRM and see when we met with them, et cetera, and look at a ratio, just be a percentage and make sure that percentage wasn’t going down because there was actually a quarter two when it went down. It actually led me to think about why is this happening. And made some corrections actually I’m in my process and my staffing as a result of that going down for two quarters. But that’s what I’m really doing is just looking at deals that are interesting to me, what fraction did I see?

There are lots of deals that may be good deals, maybe very interesting companies, maybe super successful but are not my style of investing. I personally don’t track that. I may track it for the fund and see oh yeah, this person should have met one of my partners but I never would have liked to invest even if it’s a great company because it’s just not something I care about. It’s not something that makes me passionate. It’s just not something I have insight into. I actually really care about a comparative advantage. So, very rare [inaudible 00:50:08] why invest just because I think it’s going to be a successful company. There’s usually something specific about the founder of the market, the value proposition that’s resonating with me personally to allocate my time.

Jasom Lemkin:

Founders have to remember that if you can’t take a no personally, because if it doesn’t resonate, it doesn’t resonate. There’s [inaudible 00:50:26].

Keith Rabois:

Yeah. Even if it did, I’m not sure you want to work with that person. There are times when founders tried to talk me into investing in something that’s against my business religion. Once in a while maybe I’ll consider it but it’s fundamentally, I’m not sure it’s the best for them either of like, I don’t do a component based and not staying. I don’t like components. They usually like vertically integrated businesses. Once in a while you can try to pitch me on a component based business, but I’m not sure you really want me for eight, 10 years in something that I don’t fundamentally believe in. If I know the founder already, I’ll definitely go along for the ride for people I know and I have worked with before because I can justify it from that perspective.

In fact, to answer your question, that’s basically how I find people. The best way are people that I’ve previously worked with or one degree removed from. Think of people who are funded a lot of former squares, a fair number of actually square interns have turned out to be great sources. These days in the network ages you have to go back to the drawing board. I funded people that have left DoorDash. I funded people now that have left Opendoor. You basically take your best companies with pools of pro entrepreneurs. As those people leave to go start their own companies because that’s a goal for a reasonable fraction of the pool of people at these high profile companies is hopefully they come to you first. That’s the best source.

Second source are other angel and some extensive seed fund investors. It isn’t as ideal because I want to be the first money in typically leading a seed, but I could still be Denali but those are highly qualified. That’s how we found Run The World. As I highlighted interview with business insider, two different angels in the company had simultaneously introduced me to the company and because it was two and I knew both pretty well, I think immediately responded because it was like, “Oh, well two people like this, there must be a signal there that’s interesting”.

Jasom Lemkin:

Who is a good invite.

Keith Rabois:

Yeah. I’d say, who introduced to you but also the velocity of who’s introducing you. People will reach out called though certainly through Twitter and Email. My email is public. It’s keith@foundersfund. People are happy to read emails or docs just cold or people tweet at me and occasionally there’s like a real insight in the tweet, so I’ll be happy to engage with it. Then, we do have principals in that sounded funded are pretty aggressive and looking for stuff. We don’t have that many of them, but we have like three they’re running around trying to meet interesting things, three or four actually and the flag stuff that I might’ve missed.

So for example, one of the big investments we made over this COVID virus or announced is a company in Germany called Trade Republic. That was found by one of our principals. He was super passionate and excited about that. I absolutely would’ve missed it. How do you not highlighted it for me? But once I met the company, I knew maybe 30 seconds to three minutes into the meeting that I wanted to fund it. It was so obvious that I’d met the best founder I’d ever met from Europe and I was like “How do we close this now?”

Jasom Lemkin:

Maybe just to wrap up because we’re running out of time. There’s a couple of good learnings for people to take away from that, one is, it doesn’t have to be the GP. You don’t have to get to Marc Andreessen. You don’t have to get to the very top. The folks that hustle can get you in, right? Never be condescending but here’s a perfect example. You don’t have to [crosstalk 00:54:14].

Keith Rabois:

It does depend on the fund and then promote a point about some businesses being so crazy or having so many perceived flaws. There are types of companies where that would be a bad idea and some funds where that would be about idea. So you have to cut into the fund in what company that were talking about. But this one definitely, had they come to me first, I wouldn’t have paid that much attention because Trade Republic on paper sounds like Robinhood for Europe, even though that’s not what we’re doing.

Jasom Lemkin:

That’s probably what I thought.

Keith Rabois:

I typically am not like a go invest in X for Y region investor at all. It’s incredibly inconsistent with all my philosophies wife, but it’s actually not that. The founder is extraordinary and I would not have been able to tell that had they just sent the ADAC or something.

Jasom Lemkin:

And then very last one because we’re out of time but the third one on the email. If I send you an email to keith@foundersfund. That’s the email, right? Foundersfund.com?

Keith Rabois:

Yeah.

Jasom Lemkin:

If that email is awesome, “Dear Keith, this is like Stripe but it’s better. Here’s why. We’re at 3 million in revenue. We’re growing 15% a month. We’re cashflow positive. We have no one in sales and marketing yet, and here are the four websites we power you didn’t know about.” I’m making a note but that’s a pretty good email. What are the odds you normally read an email just statistically? If I send you that [inaudible 00:55:43].

Keith Rabois:

If it is that good, very high.

Jasom Lemkin:

Very high, right?

Keith Rabois:

Yeah.

Jasom Lemkin:

That you’ll actually [crosstalk 00:55:48].

Keith Rabois:

Extremely high. Ironically, people don’t write emails like that very often. Maybe it’s not intuitive but the number of people who do not write an email even of that level is shockingly high. So if you wrote that email alone, I’d probably read it. You can tell by fonts sometimes but length, the precision, the beginning and being very clear I guess is the thing I’m really looking for. It could be in the depth or the email body but what’s special? What’s the secret? What’s special? The secret meaning like the zero to one thing that Peter talks about a lot or what’s the anomalous something? What’s the secret or what’s the anomaly? That needs to be there. If that’s clear, then I’m obviously going to pay a lot of attention. Probably take a meeting. Worst case, ask probably [inaudible 00:56:42], one of our principals to like meet the company.

Jasom Lemkin:

Yes. Let’s wrap on that but I think this is a great takeaway from Founders, privilege matters and it’s a bummer if I’m not a Square intern and I can’t reach Keith. I’m not part of that inner circle. I wasn’t at Opendoor. But the most awesome email in the world even the early metrics to back it up, it’s going to get open. It’s going to get red. It works for you. It works all the time and founders don’t get it but it has to be awesome.

Keith Rabois:

[crosstalk 00:57:13].

Jasom Lemkin:

Don’t ask for a coffee, make it awesome.

Keith Rabois:

It has to cut through the clutter, which is actually a pretty good signal anyway. If you started business from scratch, the inertia against you is pretty strong. So the ability to cut through the clutter from a value proposition to customers from potential employees is the same skill.

Jasom Lemkin:

Same skill.

Keith Rabois:

[crosstalk 00:57:31]. It actually predicts pretty well but it’s surprisingly rare how inattentive people are. I mean, again, it’s a hard skill to cut through the clutter but simple, short. Dexter better truthfully than emails because at least Dexter will tend to want to out of curiosity click through. We’re scanning emails less exciting to me. I almost always will click through a database at least really quickly and then if I see anything that snaps against a benchmark framework of what normal is, then I definitely will be intrigued and it’s going to be ideally, in the first seven or nine slides or something that snaps.

Jasom Lemkin:

Yeah. All right. Keith, this was incredible. I wish we could dig it even more but we’ve gone our full length of time. So thanks for anything. Anything else last minute you want to share? I think we’ve had some amazing stuff.

Keith Rabois:

That’s great. It’s a pleasure to be with you.

Jasom Lemkin:

All right. Stay safe and we’ll talk soon. Thanks everybody for joining.

Keith Rabois:

Great. All right.