At SaaStr, we are bullish on SaaS. I am bullish on SaaS.

And it’s hard not to be extra bullish right now. The leaders in SaaS are growing so much faster. Asana, Bill, Monday, HubSpot, etc. are all growing even faster at $200m, $400m, $1B in revenue than they did before!

That’s beyond epic, and a reason to be hyper-bullish on SaaS.

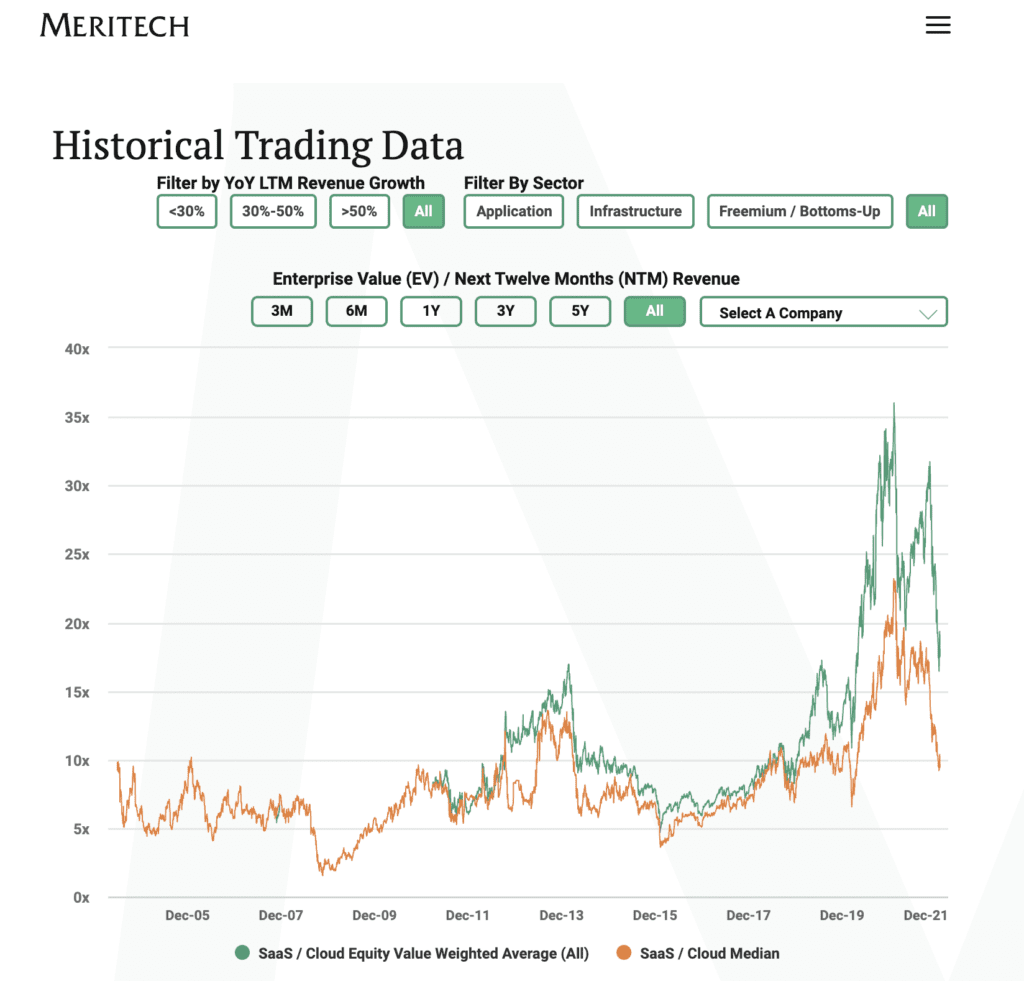

But revenue multiples might be a different story. This chart below from late-stage VC fund Meritech helps illustrate the bear case here:

Net net: median SaaS valuations are back to where they were before everyone became a SaaS investor.

I like the Meritech data not only because it’s well presented, but because you can go way back in time. Back to the early days in SaaS public companies. So far back, to 2005 and beyond, it’s probably too far back to matter today.

Yet we see trends. The #1 trend is that apart from the huge run-up in SaaS multiples starting in 2019, and a nice bump in 2012 … public SaaS companies have been trading at about 10x forward revenue.

Do they deserve more today? I would argue yes. Of course. Because they are growing faster than ever, and are better companies than ever.

But the markets right now seem to be saying we’re back or heading back to pre-2019 multiples. I hope not, and I actually don’t personally think so. I think the leaders in SaaS are just growing too fast to only have the multiples of 3-5+ years ago.

The bear multiple case, though, has a lot of historical data on its side. You can see it above. The case that Cloud and SaaS multiples, and 100x ARR rounds in venture, just got ahead of themselves.

I’m still bullish. But we’ll see.