Ok, we are facing unprecedented times. As much as 33% of the U.S. is underemployed or unemployed, or has given up looking. Our airlines are barely hanging on. Retail is imploding. Schools are closing everywhere. It’s simply terrible and unprecedented.

And yet … and yet .. these are the Best of Times for SaaS VCs. Even better than Q1’20.

Why? Two related reasons:

First, the stock market for public SaaS and Cloud companies is at an all-time high. This helps VCs raise more funds, creates more liquidity, etc. But it’s more than that.

Second, in many categories of SaaS, usage is way way up since March 15. Work from Home has been accelerated by a decade. Digital transformation by 5 years.

People are definitely starting to work in new ways. pic.twitter.com/53zY7iauud

— Aaron Levie (@levie) April 1, 2020

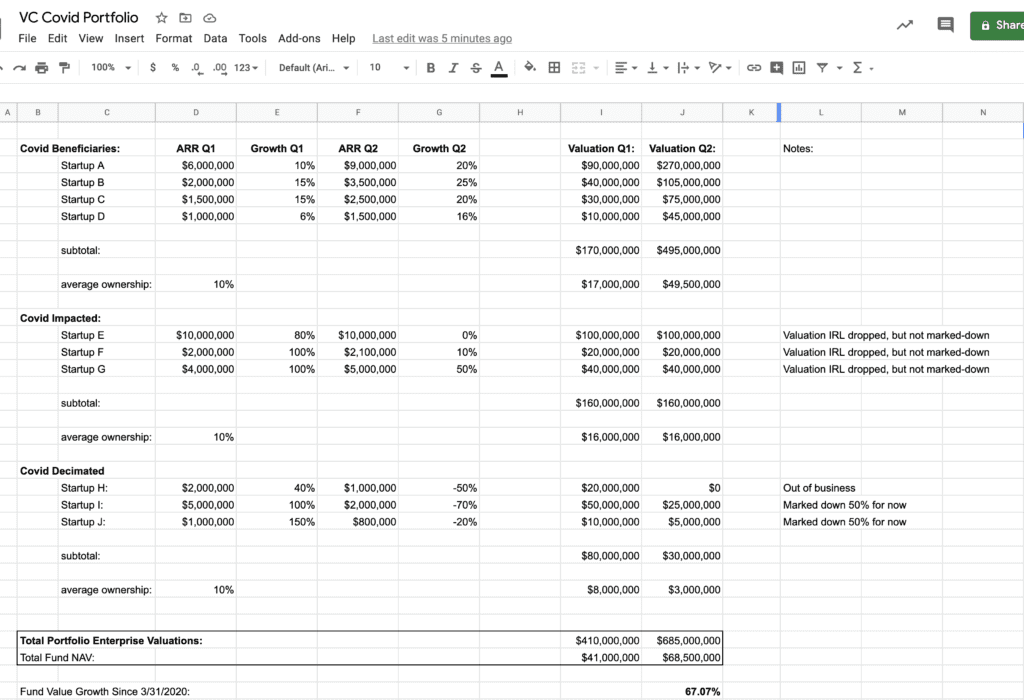

But third, and this one is a bit nonobvious — power laws mean the “Covid Beneficiaries” in most VCs’ portfolios more than outweigh the Covid Impacted and Covid Decimated. It’s a bit non-obvious, but let’s take an example of a hypothetical VC portfolio of 10 companies (to keep it simple):

- 3/10 are “Covid Decimated” in travel, events, etc. They literally have no business, or almost none, anymore. This is 30% of the portfolio. Many are now essentially worthless or close to it, at least for now, at least on paper. Certainly, most are unfundable.

- 3/10 are “Covid Impacted” and are flat or growing, but more slowly since March 15. These valuations, at best, are flat, and probably really down, but not marked down. Most are also unfundable except from insiders.

- Only 40% of the portfolio is doing better since March 15 — but they are doing a lot better as “Covid Beneficiaries”. A lot better. They now have gone from Great Companies to … Outlier Growth. These are products we need more of during Work from Home. It’s not just more Slack and Zoom. It’s more of a lot of tools and solutions. It’s contact centers and call centers. It’s tools that help us build more apps. It’s tools that facilitate collaboration and distributed project planning and remote onboarding and much more.

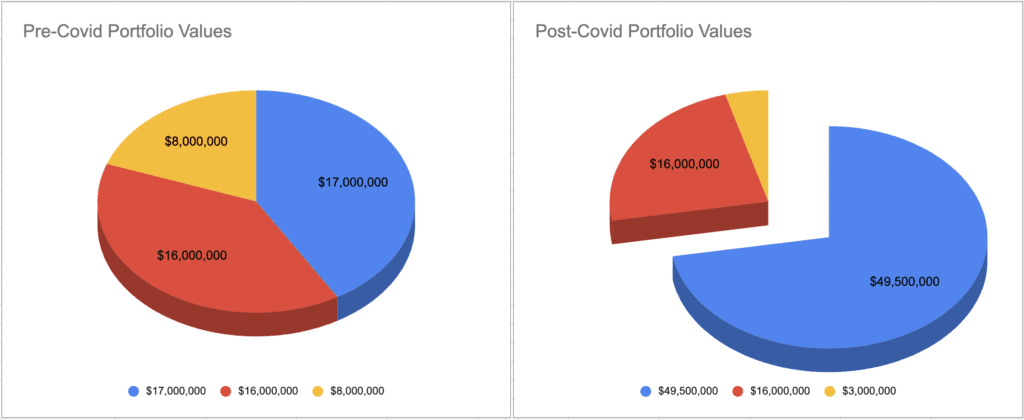

Now even though only 40% of the companies in this hypothetical VC portfolio are doing better in Cloud/SaaS since March 15, the value of their hyper-growth far outweighs the paper or real losses from the 60% that are struggling. Take a look here:

This is a bit complex, and there are a lot of assumptions here. But you see this all over TechCrunch. The ones that are Covid Beneficiaries, that are growing faster than before Covid-19, are raising huge rounds at much higher prices. Because they are growing even faster in these crazy times

In our example over, the 3 “Covid Beneficiaries” have added $32,000,000 in gains to this fund (Blue), and thus a 67% total fund-level gain since March 15. Even with 60% of the portfolio really struggling (Red) or even going under now (Green):

Power laws are a strange thing. Even stranger in strange times.

So net net:

- VC $$$ are back in SaaS (they barely went away) — but they are only funding Covid Beneficiaries. Why would you invest anywhere else?

- It’s very hard to get funded if you aren’t growing faster than in March. Is this fair? No. But VCs only want to invest in the 4/10 in the above portfolio.

- For now, at least — SaaS VCs are benefitting from these crazy times. But can it last? We will see.

things I didn't expect:

– massive acceleration of growth of disruptive companies across many categories (> 100% y/y growth)

– after 6 weeks VC funds starting pouring cash back in due to above, now tons of $

– public markets hold (gov't $ + new retail investors)— Mark Suster (@msuster) July 30, 2020