TechCrunch yesterday published a short post we did explaining why now, Box will clearly get to $1,000,000,000 in ARR, once it IPOs.

There’s so much controversy around the space, and Box. But for us SaaStrs, it’s just an example of how recurring revenue models work at scale. No matter what the product does, really.

The post at TechCrunch here and below.

Editor’s Note: Jason Lemkin is a managing director at Storm Ventures focusing on early stage software as a service and enterprise software startups.

There’s probably no enterprise software company more people opine on than Box. In particular, the business model of Box. They’re spending so much, Alex says. I like Google Drive better,Ron says. File sharing is a commodity, Jon says.

They’re all right, on some level.

But while opinions are somewhat subjective, math is math, and the physics of software as a service (SaaS) and recurring revenue are highly predictable. And there’s one thing we now know after Box’s recent SEC filings on its run up to an IPO: Box will be at a billion dollars in revenue before we know it. In fact, probably right around 2019.

And this has absolutely nothing to do with what you or I think of Box as a product, or even what you think about the market per se.

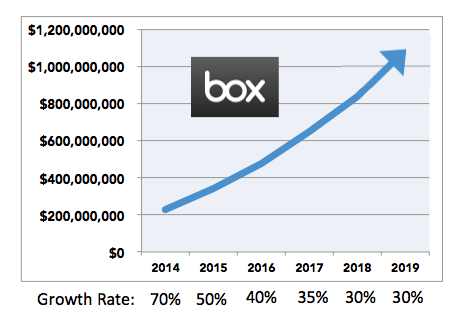

Here’s what Box’s revenue run rate is today, and will it look like over the next 5 years, based on current and projected growth rates (Box hit a $228,000,000 run rate in Q3):

From Box’s SEC filings, we can predict the future pretty reliably. Even if growth dramatically declines, Box will still hit a $1,000,000,000 revenue run rate by 2019. Box’s growth rate declined a bit in Q3 ‘14, but it’s still growing at an epic rate — 70 percent year-over-year in 2014.

-

If this gradually declines to 30 percent growth by 2019 — a much lower growth rate than comparable companies like Salesforce experienced at this stage — Box will still cross a $1,000,000,000 run rate in 2019. This is just basic math, the way recurring revenue compounds.

-

Box no longer has any material risk of ever running out of money. In Q3, Box’s magic number decreased from 1.38 to 0.97. In other words, Box now spends less than its first year of customer revenue acquiring and closing its customers. As long as this continues to decline, Box’s losses will decline as well.

-

Add in, say, $250 million from an IPO, and Box should never run out of money. That might have been a risk before Box added an additional $150 million in funding earlier this year, and before sales and marketing expenses declined. But unless an IPO never comes, Box has, for all intents and purposes, infinite cash runway now.

-

The customers are all still renewing. As they almost always do with true Enterprise products. One objection to Box’s business model is the general concern that cloud storage is commoditized to the point of free.

-

File storage may now be free, but clearly, the customers are still renewing. And customers aren’t stupid. They clearly view the enterprise-grade functionality of Box as worth quite a lot. If churn had dramatically grown, the growth rate above could be at risk. But churn isn’t materially growing, according to the latest SEC filings.

-

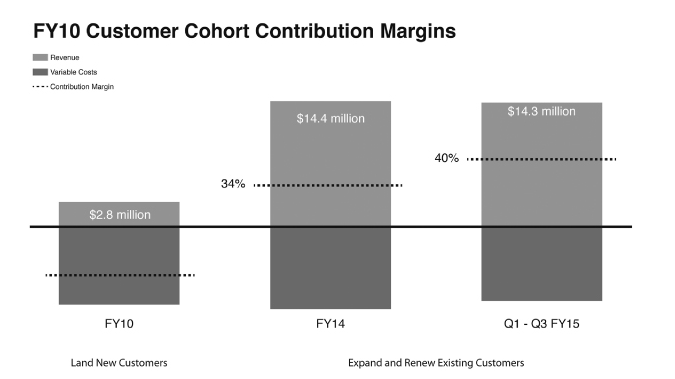

Box’s customers continue to buy more Box, and pay more for Box, in the second and third years after first buying. This isn’t just true of Box. It’s nothing special. It’s exactly what we’d expect. Because it’s true of all true enterprise SaaS companies. No matter what their products do:

You can love Box, hate it, or maybe never even use it but still have an opinion. It’s fun water-cooler talk. But SaaS and recurring revenue is highly predictable once you hit scale. Box will hit a $1 billion run rate around 2019, plus or minus.

You can bank on that.