One of the most powerful things in SaaS is having a visionary founder-CEO. Nothing against an outside CEO. Sometimes, the time comes to hand the baton to someone else.

But, but — only a founder CEO can execute a vision over 20+ years. Only a founder CEO knows the why. Only a founder CEO is always, forever, a founder. Jobs come and go. But whatever company you found, you are its founder forever.

So an interesting case study is Blackline. After an incredible run as a solo female founder, Therese Tucker moved to the board a few years back. But when they needed that founder DNA, Therese came back last year. As CEO again.

Blackline is one of the leaders in accounting software and invoicing-to-cash. But the ACV as we’ll see is small, and the competition is real. Growth got tougher. They needed Therese back.

Attention founders: you might be asked back as CEO some day, too.

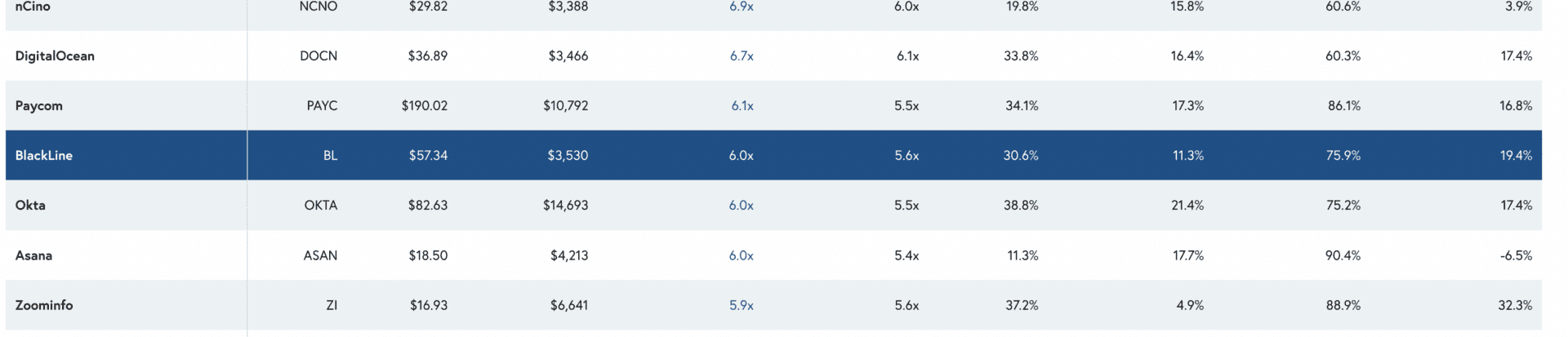

Today, at $600m ARR, Blackline’s market cap — is right in the middle of SaaS leaders. It’s trading at 6x ARR. $3.5 Billion. Ahead of Asana and Box, and just behind Freshworks and DigitalOcean. Good company. 6x is the average today for leading public companies.

5 Interesting Learnings:

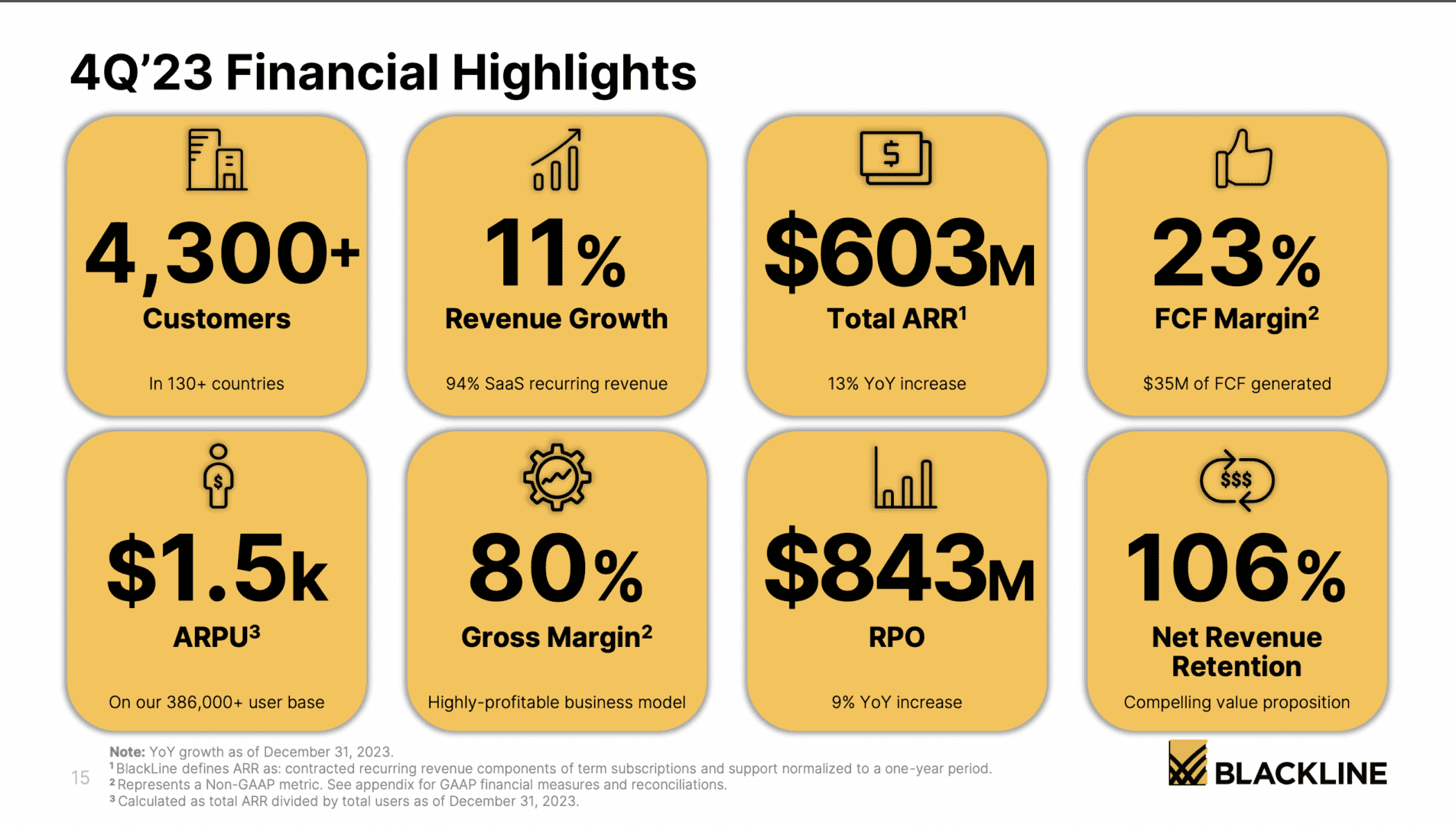

#1. Growth Has Slowed to 11%, But It’s Efficient, With 23% Free Cash Flow Margins

Blackline’s growth has slowed and is approaching the “mature” phase, at just 11% annual growth on 106% NRR. But it’s gotten pretty darn efficient to make up for it, with 23% free cash flow margins.

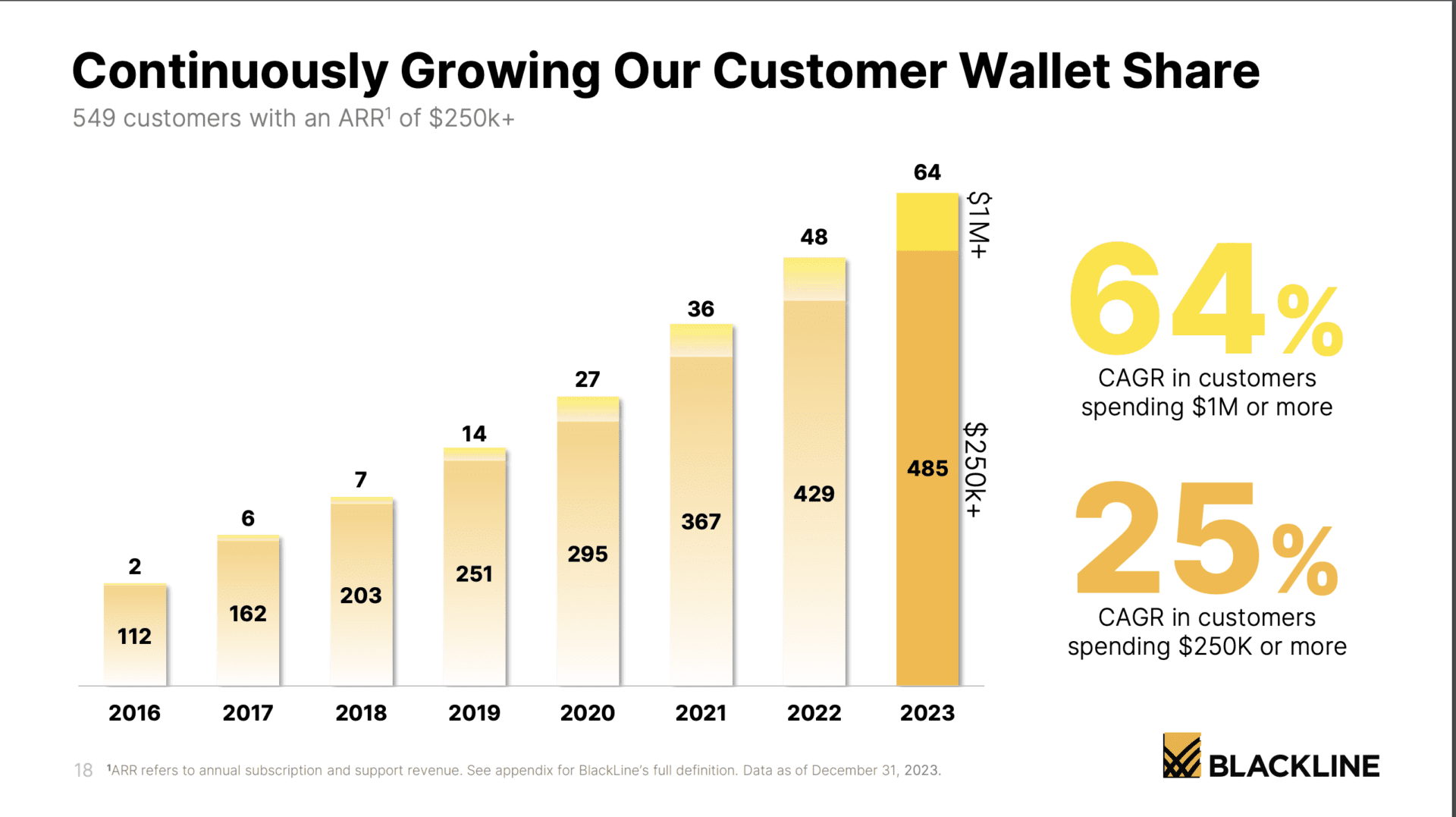

#2. $140k Average Deal Size, With The Real Growth in $250k+ and $1m+ Accounts

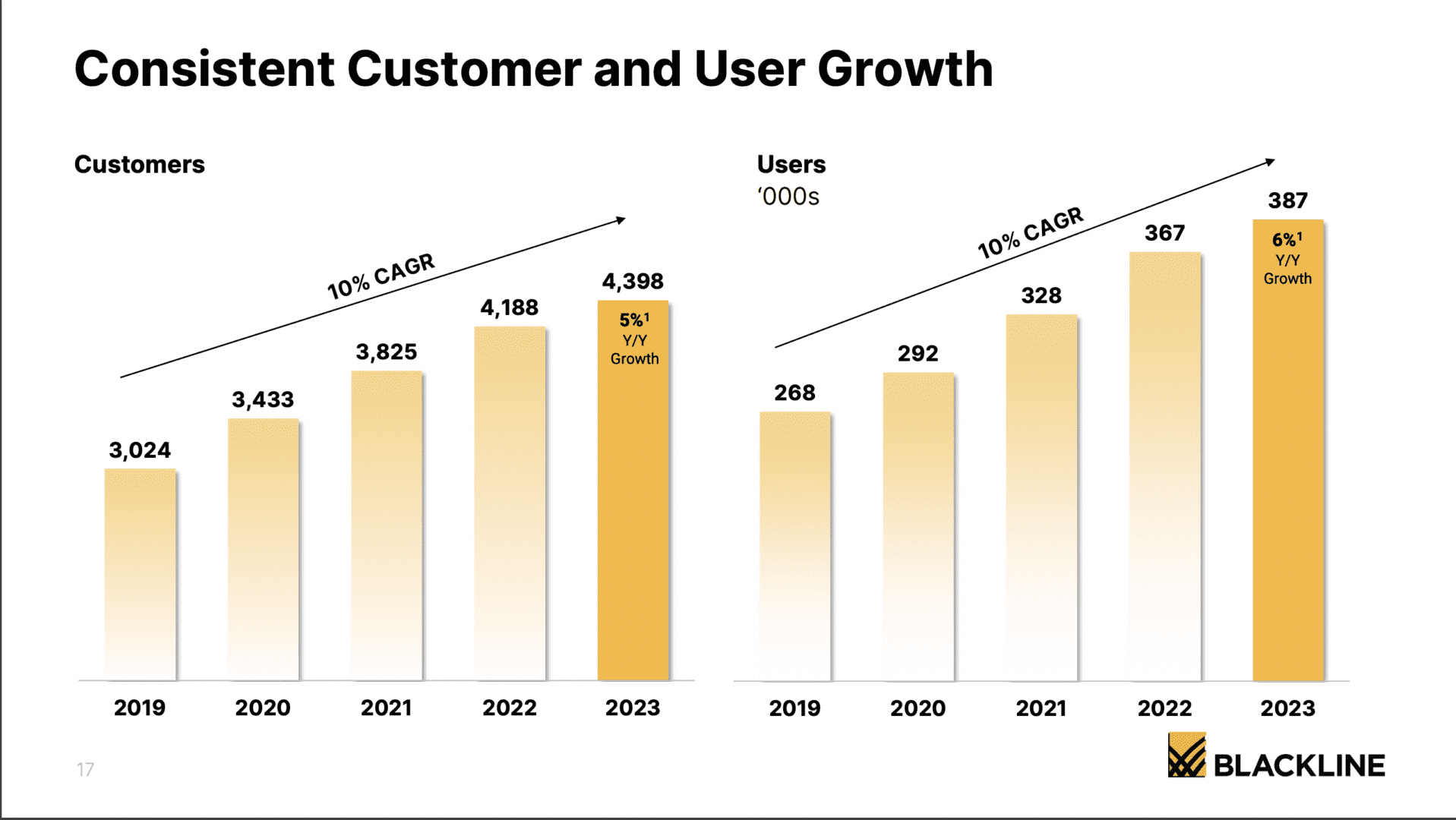

With 4,300 customers and $600m in ARR, Blackline’s average customer pays about $140k per year. But it’s the even bigger ones that drive growth. Their $250k accounts are growing 25% and $1m+ accounts 64% a year. 549 customers pay $250k+ a year or more, and 64 pay $1m or more.

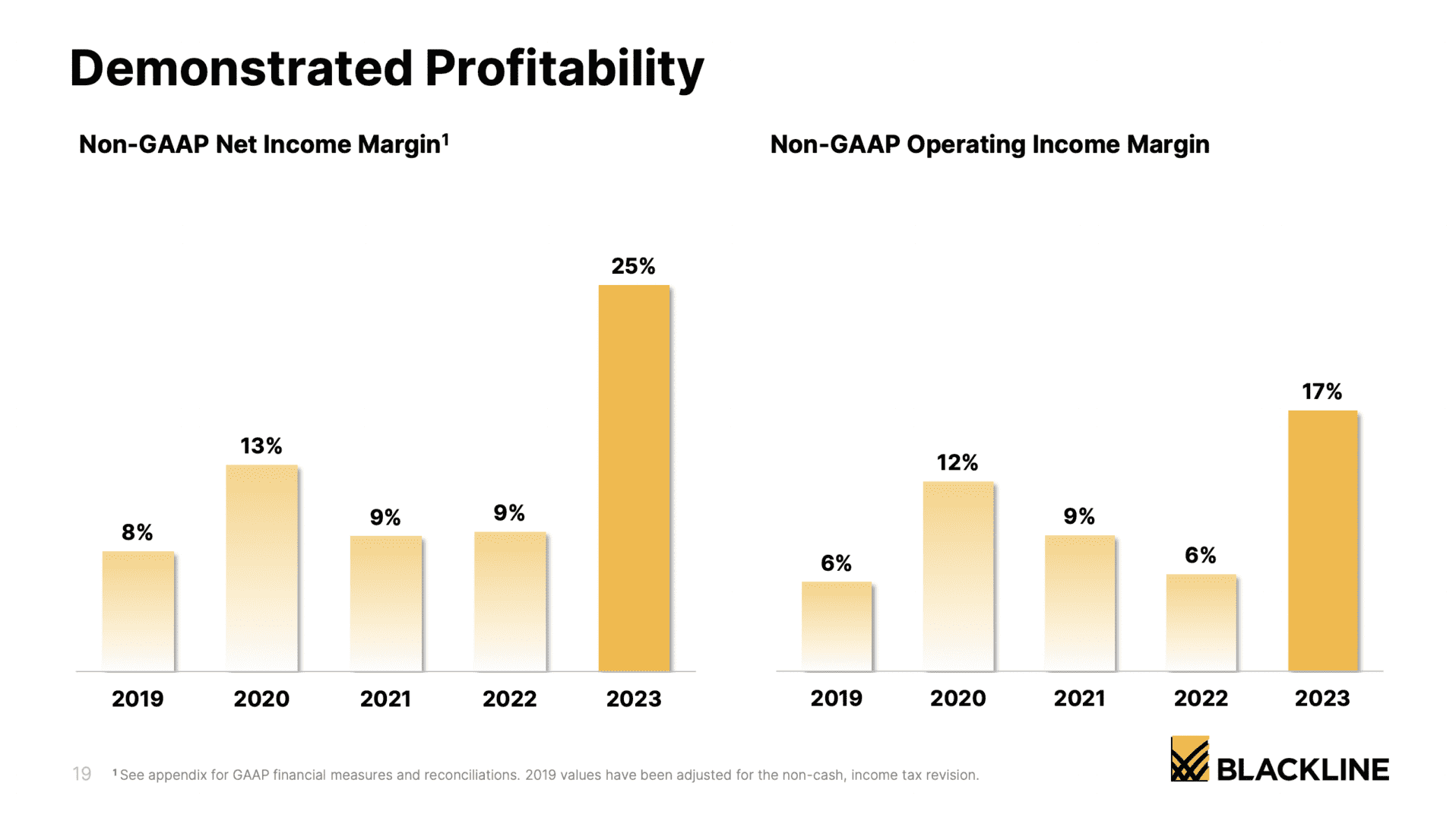

#3. Like Almost Everyone, They’ve Gotten Much More Efficient

The theme of the day. Blackline has been cash flow and net income positive for years. But the times have changed, and folks are being asked to be even more efficient. Blackline responded, and his record operating and net income margins in 2023.

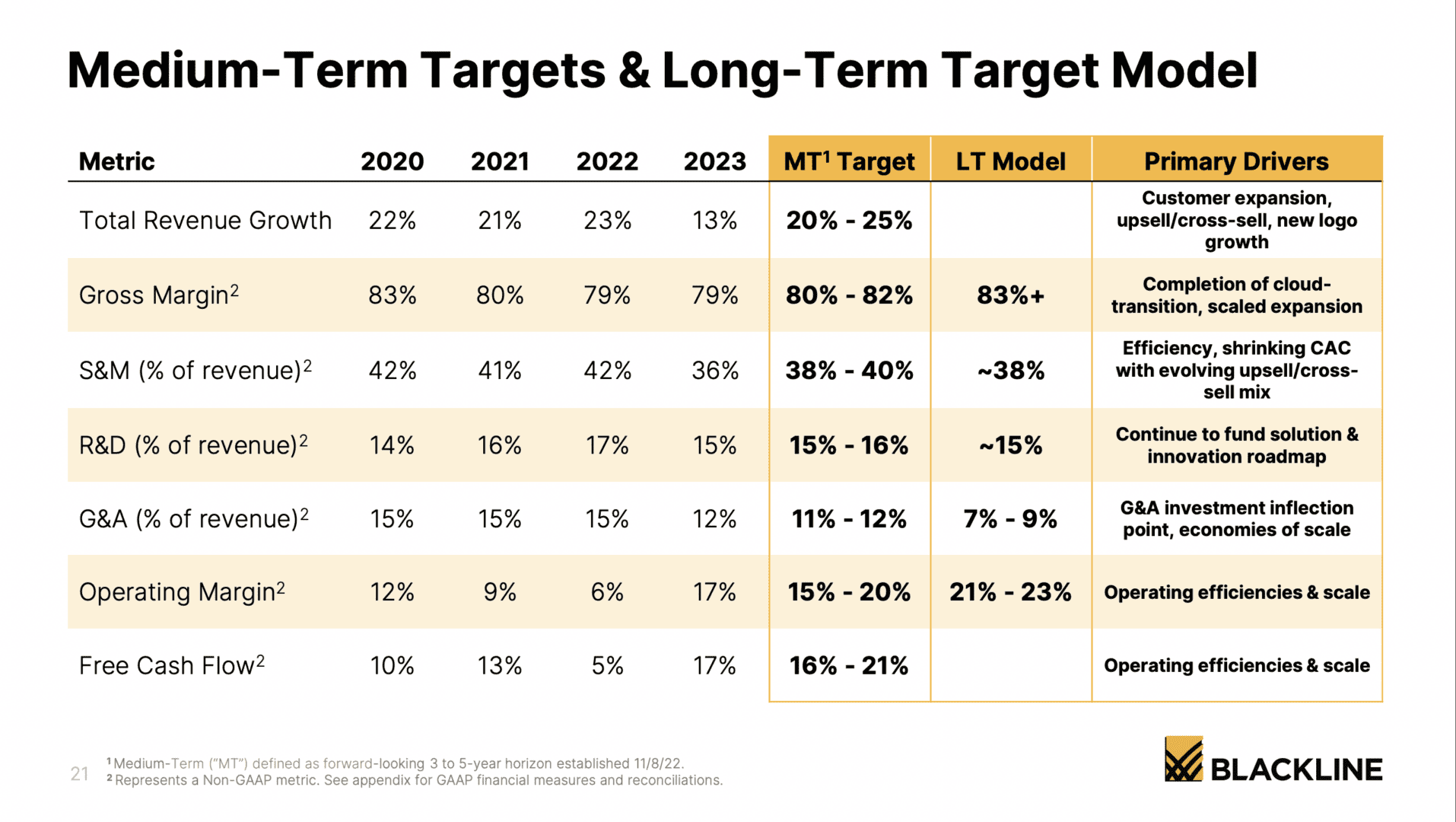

#4. 2023 Was Tough, But Predicting a Return to 20%+ Growth

I love the boldness here with Therese back as CEO. Blackline had consistent growth of 20%+ in 2020, 2021, and 2022. Then 2023 was tough, and Therese came back. And they’re putting it out there — they will get back to 20%+ growth. They’re not settling for an “end state” of mature software. Love it!

#5. NRR Has Slipped a Bit from 109% in 2022 to 106% Today — But Not All That Much

Enterprise spend really does hold up. And Blackline noted it has seen a slight increase in NRR recently.

And a few other interesting learnings:

#6. 5% Customer Growth + 106% NRR = 11% Revenue Growth

Super helpful when the math ties here 🙂

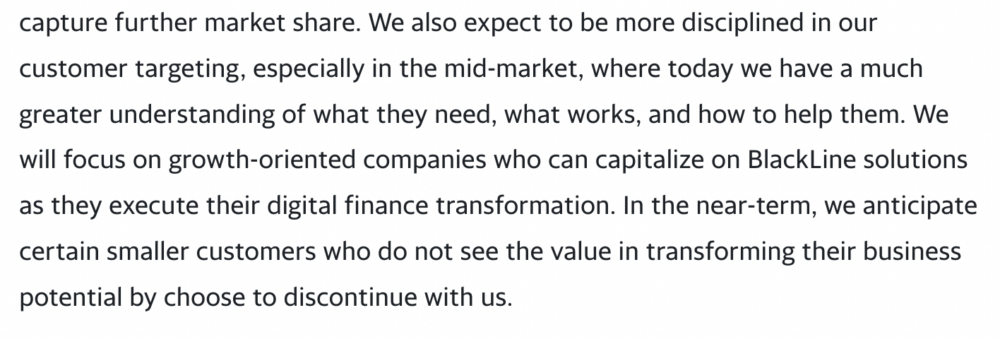

#7. Leaving Some of Its Smaller Customers Behind

As Blackline standardizes around $250k+ deals as growing mid-market and enterprise companies, it’s found its tough to support the smaller ones.

#8. 94% GRR

Blackline may not have top-tier NRR, but it does have top-tier GRR at 94%. Folks stay. Getting even better at getting them to buy even more from Blackline will help accelerate growth.

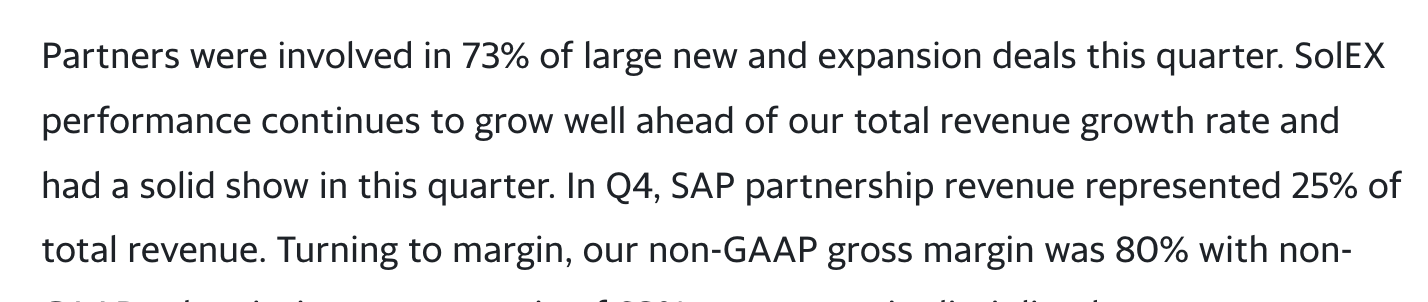

#9. Partners Involved in 73% of Deals, and SAP Partnership Was Responsible for 25% of Revenue

Way too many founders and VPs of Sales are 100% focused on selling direct. But partners are so key in so many industries. With SMBs, HubSpot and Shopify both get 40% or so of their customers from small partners and agencies. With Blackline, it’s much more enterprise, with folks like SAP influencing or driving 73% of deals. Sell only direct, and the competition may box you out.

And a great deep dive with founder CEO Therese Tucker on truly going long here: